Prices May Have Peaked--For Now

Prices of commodity resins were on the way up last month, driven by higher feedstock costs and restricted supplies of feedstocks and resins.

Prices of commodity resins were on the way up last month, driven by higher feedstock costs and restricted supplies of feedstocks and resins. But most prices may be at or near their near-term peaks. In the case of PP, there is a likelihood of a sharp drop from recent highs. Polystyrene prices, however, are projected to be flat-to-upward, according to purchasing consultants at Resin Technology, Inc. (RTi) in Fort Worth, Texas (resinpros.com). Here’s more of their analysis and predictions.

PE PRICES UP, BUT PEAKING?

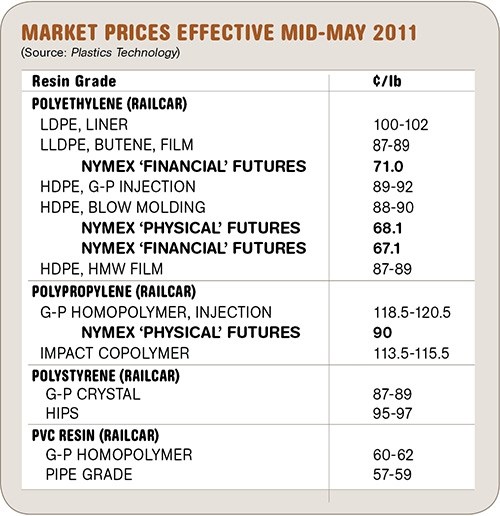

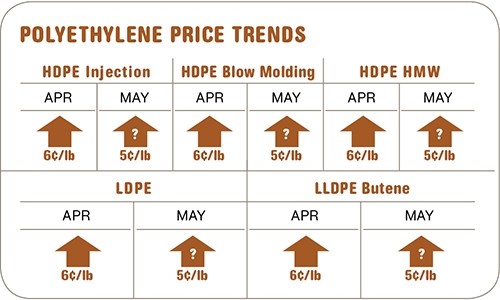

Polyethylene prices moved up 6¢/lb in April, bringing total increases implemented this year to 11¢. There was a 5¢/lb hike pending for May, but its fate appeared uncertain by mid-month. Suppliers issued a range of price hikes for June 1, from 4-6¢/lb for LL/LDPE to 8¢ for HDPE. One supplier issued 2¢/lb for LL/LDPE in June and 4¢/lb more for July.

Similar to 2010, this year is shaping up to be a seller’s market globally. Many grades are sold out, and HDPE was on allocation from March through May. The problem is production outages and availability of ethylene monomer to make PE.

Domestic demand through March and into April was up 10%, some of it due to prebuying ahead of price increases. But processors are having difficulty passing the PE price hikes downstream. The secondary market was active in March and April, but at near-prime pricing levels due to limited availability. Last month started showing signs of some loosening in supply.

Outlook & Suggested Action Strategies

30-60 Days: Tight supply and elevated monomer prices put upward pressure on resin prices last month. But higher PE price levels could result in some demand destruction. May could be the peak for PE prices, but they probably won’t go lower. Buy as needed for June/July. Nine PE and four ethylene plant maintenance turnarounds are scheduled in the next couple of months, which will likely tighten supplies. PE prices should remain flat in the second half, with no more than another 5¢ increase likely to stick.

PP PRICES UP, BUT COULD DROP

Polypropylene prices moved up 15¢/lb in April, in step with propylene monomer, which moved to a new record high of 87.5¢/lb, owing to short supply and production problems. Suppliers issued PP price hikes of 10¢ to 15¢/lb for May, anticipating similar monomer price increases. But May propylene prices settled only 7¢ higher, so PP prices are moving accordingly. Monomer cost and availability are big drivers of resin prices.

Broad swings in PP prices have had an inverse effect on demand. In March, domestic resin demand was up by nearly 40%; ditto for PP plant operating rates, which increased by over 21% to the low 90s. However, demand was moving downwards again in April and more significant demand destruction was anticipated by end of May. Supplier inventories dropped to 33 days in April from 39 days in February. Overall domestic demand in 2011 is down 6.6% from 2010, while export demand is off by 4.2%.

Outlook & Suggested Action Strategies

30-60 Days: May prices were expected to be at or near peak levels. Watch sales in the spot market for resistance to the higher prices. PP prices could fall significantly, even by double digits, through this month and remain flat until the latter part of the year. The possibility of double-digit price hikes later in the year cannot be ruled out. The PP market is so tightly balanced that any unforeseen event can tip it either way. A lot depends on what happens to resin demand and to monomer availability.

PS PRICES UP

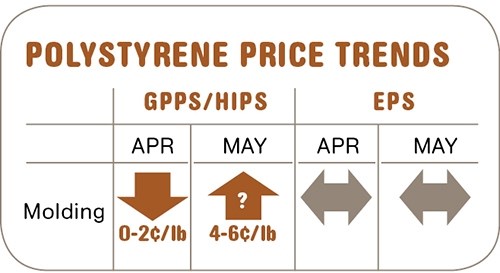

Polystyrene prices were moving up in May, though initial offers of 5¢/lb for GPPS and 10¢ for HIPS were being negotiated downwards—i.e., 4¢/lb for GPPS and 6¢/lb for HIPS. The delta between GPPS and HIPS has grown to 11-12¢/lb due to the high cost and tight supply of butadiene.

Price volatility and healthy demand for GPPS, HIPS, and EPS have created a tighter supply situation and the need to forecast your resin needs. Ineos has had difficulty delivering PS due to two downed resin units. Total has been trying to make up the gap.

Styrene monomer contract prices in April dropped 3-4¢ to 64-65¢/lb, but spot prices were as high as 68-69¢/lb. May styrene contracts were expected to settle 3-4¢ higher. Meanwhile, April butadiene contracts settled up 17¢ to $1.21/lb—a 16% increase that amplified the GPPS-HIPS price spread. Spot prices were as high as $1.71/lb and speculation on May butadiene contracts was for an increase of more than 20¢/lb.

Outlook & Suggested Action Strategies

30-60 Days: With May prices on the increase, and availability continued tight, PS and EPS prices will be flat-to-upward. Buy as needed. Prices will probably abate in the late third quarter due to seasonal falloff in demand.

PVC PRICES RISE

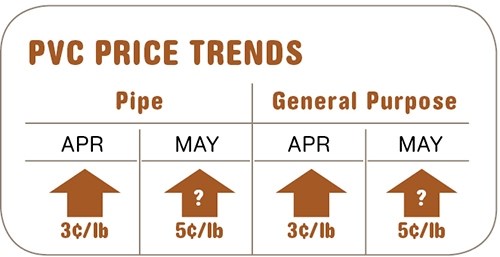

PVC prices moved up 3¢/lb in April and there was a 5¢ increase on the table for May. Key drivers included increased global demand and supply problems both here and abroad.

Georgia Gulf is continuing force majeure from its Plaquemine, La., plant, citing ethylene supply and chlorine operating issues. Two PVC producers were down through May for maintenance turnarounds. Formosa claims to be on track with an expansion that will add more than 500 million lb/yr of PVC to the market later this year.

U.S. exports have risen since the earthquake disrupted 1.5 billion lb of capacity in Japan. But those exports began to meet with resistance at the higher May price levels.

Outlook & Suggested Action Strategies

30-60 Days: May prices were expected to move up—although weakening exports made it uncertain that the full 5¢/lb would be implemented. Expect supply relief from restarted Japanese capacity along with improved production from Georgia Gulf and Formosa. Buy as needed. Prices this month are expected to be flat, with opportunities for reduced prices in the third quarter. Ethylene production reliability and the strength of the construction season will be key drivers.

Related Content

The Fundamentals of Polyethylene – Part 2: Density and Molecular Weight

PE properties can be adjusted either by changing the molecular weight or by altering the density. While this increases the possible combinations of properties, it also requires that the specification for the material be precise.

Read More

The Fundamentals of Polyethylene – Part 1: The Basics

You would think we’d know all there is to know about a material that was commercialized 80 years ago. Not so for polyethylene. Let’s start by brushing up on the basics.

Read More

Melt Flow Rate Testing–Part 1

Though often criticized, MFR is a very good gauge of the relative average molecular weight of the polymer. Since molecular weight (MW) is the driving force behind performance in polymers, it turns out to be a very useful number.

Read More

Fundamentals of Polyethylene – Part 6: PE Performance

Don’t assume you know everything there is to know about PE because it’s been around so long. Here is yet another example of how the performance of PE is influenced by molecular weight and density.

Read MoreRead Next

Why (and What) You Need to Dry

Other than polyolefins, almost every other polymer exhibits some level of polarity and therefore can absorb a certain amount of moisture from the atmosphere. Here’s a look at some of these materials, and what needs to be done to dry them.

Read More

Lead the Conversation, Change the Conversation

Coverage of single-use plastics can be both misleading and demoralizing. Here are 10 tips for changing the perception of the plastics industry at your company and in your community.

Read More

How Polymer Melts in Single-Screw Extruders

Understanding how polymer melts in a single-screw extruder could help you optimize your screw design to eliminate defect-causing solid polymer fragments.

Read More