Prices of PP, PS Up, Flat for PE & PVC--For Now

The second quarter will bring a risk of higher prices for PE, PS, and PVC, driven primarily by higher feedstock costs and a strong rebound of exports.

The second quarter will bring a risk of higher prices for PE, PS, and PVC, driven primarily by higher feedstock costs and a strong rebound of exports. In contrast, PP prices were already softening last month following an unprecedented run-up spurred by monomer cost increases. A price correction for both is projected within the next couple of months. That sums up the outlook from resin purchasing consultants at Resin Technology, Inc. (RTi) in Fort Worth, Texas.

PP PRICES ON A YO-YO

Polypropylene prices surged a whopping 17¢/lb in January, following similar increases for propylene monomer. Some suppliers issued a new 3¢ hike for Feb. 1, based on signs that monomer would rise by that amount. However, February monomer prices stayed put at 77.5¢/lb.

Spot prices for both resin and monomer were sliding a bit by mid-February. Given a drop in demand and some improvements in supply, the monomer situation was showing a better balance over the previous month. Not surprisingly, demand for PP sank following the price increases. This was reflected by lower price offers in the secondary market. In response, PP suppliers began cutting production rates even more (rates had already dropped to 83.5% by early January from September’s 90%). Nymex PP futures indicate an expected sharp drop in prices.

Outlook & Suggested Action Strategies

30-60 Day: Monomer supply will continue to improve. A price correction could take two to three months for both monomer and resin. Buy as needed. This is not a good time to stock up, as further price erosion is expected. Prices could drop sharply in March—even by 10¢/lb or more.

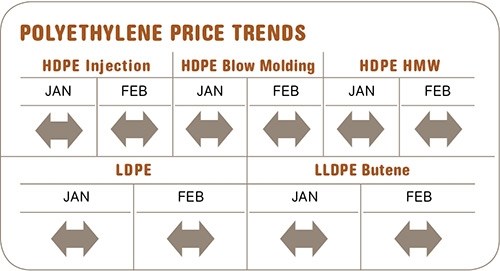

PE PRICES FLAT FOR NOW

Polyethylene prices remained flat through January, despite announced December/January price hikes that totaled 11¢/lb. Suppliers did issue a new 5¢ hike for Feb. 1, though some delayed 2¢ of it to March. There were no major market indicators supporting higher prices, but the situation is fluid: At press time, Dow, ExxonMobil, and LyondellBasell reported shutdowns and were putting customers on allocation.

Spot ethylene monomer prices were 44-47¢/lb in mid-February, up from 41-42¢ in mid-January, spurred by weather-related production disruptions. After the latest shutdowns, spot ethylene shot up to 53¢/lb. While ethylene supply was much improved in January, the situation appears to be changing. Several production units are also slated to go down for plannned maintenance in the next two months.

PE suppliers say the market is tight. But domestic and export demand has been flat, and increased material availability is reflected in a strong spot market with substantial discounts. Average days of inventory are at 29 days, where they have been for two years.

Outlook & Suggested Strategies

30-60 Day: Supply disruptions and an increase in exports are the two factors that could push PE prices up. Buy as needed.

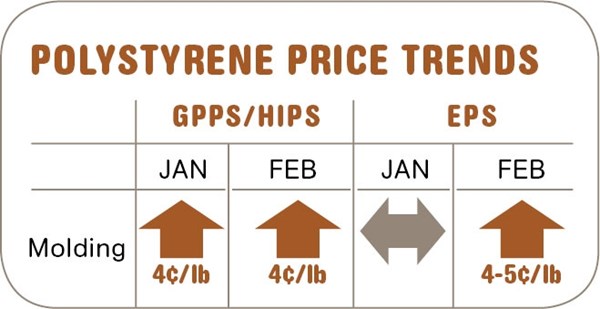

PS PRICES UP

Polystyrene prices moved up 4¢ in January and another 4¢ in February, mirroring movements in styrene monomer contract prices, which settled at 65¢/lb in January and were poised to rise 4-5¢/lb for February. Continued increases in benzene prices and tight monomer supplies have been the key drivers.

As had been expected, butadiene contract prices in January moved up 5¢ to 91¢/lb. February contract prices were poised to jump another 9¢, driven by strong global demand compounded by poor supplies of natural rubber in Asia. Prices have soared by 28% within a three-month period and are expected to remain at very high levels for most of the year.

U.S. PS prices are the highest in the world. Through January, GPPS had risen 9¢/lb over six months. HIPS commands an 8-9¢/lb premium over GPPS.

Outlook & Suggested Action Strategies

30-60 Days: We suggested stocking up to cover your inventory needs through April. Prices should peak in February/March, with HIPS prices expected to remain above the normal premium over GPPS, due to the cost of butadiene. Review your prices in relationship to the rest of the market, as price variances have increased as prices climbed.

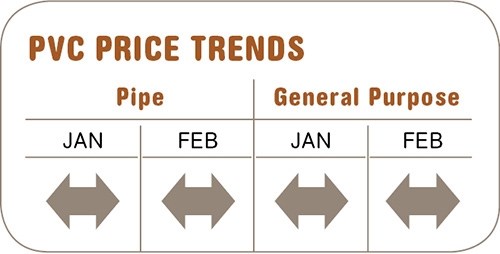

PVC PRICES STILL FLAT

PVC prices in February were flat for a third month, and the announced January 3¢/lb increase did not take effect. Suppliers were expected to attempt another increase last month, both as a hedge against unplanned cracker outages and the potential for revival of strong Chinese export demand by March.

Domestic demand dropped about 13% since last Fall, leaving resin plant operating rates in the 75% to 79% range by February. Exports to China came to a halt during the Lunar New Year holidays, but could now resume. Adding to an already well-supplied market is Formosa’s 240-million-lb capacity expansion slated for start-up this month.

Outlook & Suggested Action Strategies

30-60 Day: In January, we suggested purchasing as needed while looking for lower price opportunities through mid-February. Asian supply/demand balance after the Lunar New Year is the open question, with some traders betting on a strong recovery in demand for the rest of the year. While exports could drive the market higher starting this month, that is hardly certain. Anticipate ample supplies to influence the market at least through the first part of this quarter. Buy as needed.

Related Content

Melt Flow Rate Testing–Part 1

Though often criticized, MFR is a very good gauge of the relative average molecular weight of the polymer. Since molecular weight (MW) is the driving force behind performance in polymers, it turns out to be a very useful number.

Read More

Understanding the ‘Science’ of Color

And as with all sciences, there are fundamentals that must be considered to do color right. Here’s a helpful start.

Read More

The Effects of Time on Polymers

Last month we briefly discussed the influence of temperature on the mechanical properties of polymers and reviewed some of the structural considerations that govern these effects.

Read More

The Importance of Melt & Mold Temperature

Molders should realize how significantly process conditions can influence the final properties of the part.

Read MoreRead Next

Understanding Melting in Single-Screw Extruders

You can better visualize the melting process by “flipping” the observation point so that the barrel appears to be turning clockwise around a stationary screw.

Read More

Advanced Recycling: Beyond Pyrolysis

Consumer-product brand owners increasingly see advanced chemical recycling as a necessary complement to mechanical recycling if they are to meet ambitious goals for a circular economy in the next decade. Dozens of technology providers are developing new technologies to overcome the limitations of existing pyrolysis methods and to commercialize various alternative approaches to chemical recycling of plastics.

Read More