Trending Up Despite a Slip

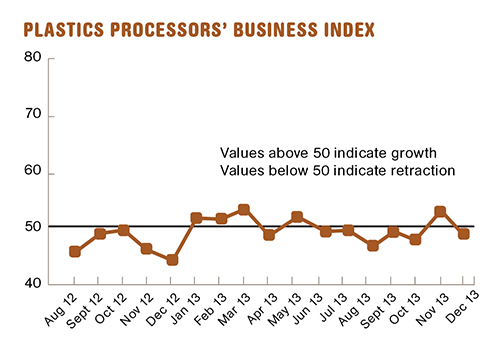

Despite a slip in December, processors are still generally doing much better now than a year ago.

.JPG;width=70;height=70;mode=crop;format=webp)

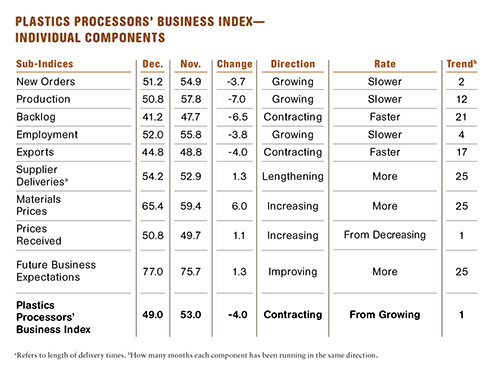

With a reading of 49, Gardner’s Plastics Processors’ Business Index contracted for fourth time in five months. But that’s a bit misleading, because during that period of contraction, the trend of the index has been rising. More to the point, in four of those same five months the index has been higher than it was one year ago. In the last two months, the month-over-month rate of change has been above 11%. Bottom line: Processors generally are doing significantly better now than they were a year ago.

New orders grew for the third time in four months. While production grew significantly slower in December, production in fact increased every single month in 2013. Generally, production has been growing faster than new orders. Therefore, backlogs continue to contract, although that rate of contraction has slowed somewhat. This could be a positive sign for capacity utilization. Employment grew for the 11th of the last 12 months. Exports have contracted at a relatively constant rate since the fall of 2012. And supplier deliveries have lengthened at a faster rate since September 2013.

For most of 2013, material prices increased at a slower rate. However, that trend was clearly broken in December as material prices increased at their fastest rate since March. Prices received increased somewhat for the first time in two months. Future business expectations have increased sharply since October, reaching their second highest level in the history of the index.

Plants with more than 50 employees had been growing for several months. But in December, only those with 100-249 employees grew. Facilities with that many workers grew every month but two in 2013. Plants with 50-99 and more than 250 employees contracted for the first time in two months.

The Pacific region grew for the fourth time in five months. And the East North Central region grew for the third time in four months. These were the only two regions to grow in December.

Future capital spending plans were above $1 million per plant for the fourth straight month. But for the first time in the history of the index, the month-over-month rate of change was negative. Spending plans in December 2013 were 10.3% lower than a year ago. But the annual rate of change is still growing at 34.4%. It still looks like processors intend to buy more capital equipment in 2014.

ABOUT THE AUTHOR

Steven Kline Jr. is part of the fourth-generation ownership team of Cincinnati-based Gardner Business Media, which is the publisher of Plastics Technology. He is currently the company’s director of market intelligence. Contact: (513) 527-8800; email: skline2@gardnerweb.com; blog: gardnerweb.com/economics/blog.

Related Content

-

Plastics Processing Expansion Continues

March marked the fourth straight month of gains.

-

Plastics Processing’s Ups and Downs

Overall index dips, but custom processors hold steady. Employment up, backlogs down.

-

NPE2024 and the Economy: What PLASTICS' Pineda Has to Say

PLASTICS Chief Economist Perc Pineda shares his thoughts on the economic conditions that will shape the industry as we head into NPE2024.