Commodity Resin Prices Heading Up

Upward pressure on prices comes from production disruptions and higher feedstock costs.

The trajectory for PE and PP prices is definitely upward for now, as planned and unplanned resin and feedstock production disruptions have tightened supplies significantly. Spot-market material is scarce, and traders with material have been ratcheting prices higher.

Prices of PS moved up too, but some relief was possible as feedstock costs and availability may improve. Meanwhile, PVC suppliers were aiming to hike prices as well, but the outcome remained unclear as processors pushed back. These are the observations of purchasing consultants at Resin Technology Inc. (RTi), Fort Worth, Texas, and CEO Michael Greenberg of The Plastics Exchange, Chicago.

PE PRICES HEADED UP

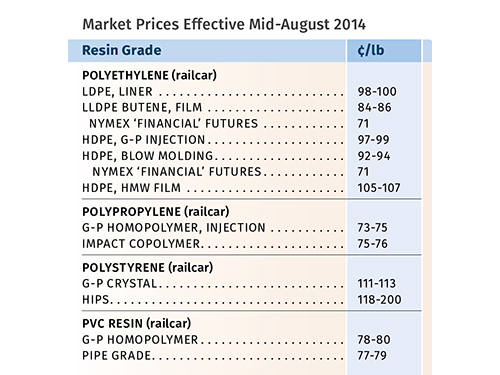

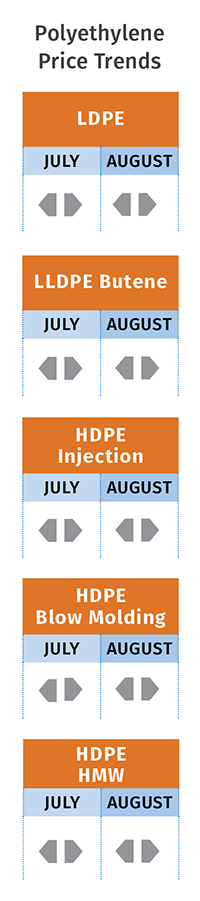

Polyethylene prices are generally expected to rise this month, with most suppliers except Nova Chemicals seeking increases of 3-4¢/lb. July production disruptions fueled a resin-buying frenzy, with buyers of both prime and off-grade resins focusing on covering their needs through October, according to Mike Burns, RTi’s v.p. for PE.

While LyondellBasell removed its resin allocation on Aug.1, CPChem had not restarted its plant, and allocation was expected to remain through August. According to Burns, CPChem’s HDPE availability is a major concern as fall approaches. Meanwhile, Dow alerted its customers to a “serious” plant disruption in Canada on July 31, with some processors

notified of major allocations—as little as 50% of their August orders. It now appears that nearly everyone is on order control. “You can only get what you normally buy,” observed Burns, adding that LL/LDPE supplies are tight but HDPE availability is even worse. He added that inventory recovery is not expected for at least 60 days.

Spot PE trading was swift and prices continued to rise through July into August. A change in market sentiment encouraged modest restocking, which, coupled with several recent resin production issues, quickly drove up spot market prices by as much as 5-7¢/lb. Spot supplies of LDPE and LLDPE film grades remain snug while offers for HDPE appeared to have disappeared, according to Greenberg.

PP PRICES REBOUND

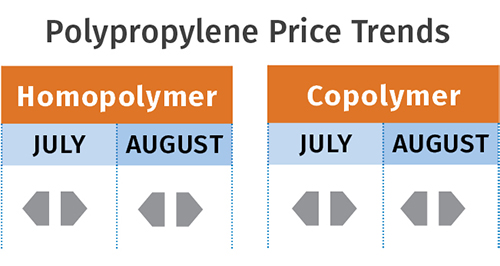

Polypropylene prices were expected to move up last month in step with proposals for a 6-7¢/lb monomer increase, driven by unplanned production disruptions at several crackers. At least three PP suppliers—Phillips 66, Ineos, and Pinnacle—gave notice of their intentions to hike PP prices and tack on additional increases of 2-4¢/lb for margin expansion above the final August monomer contracts, according to Scott Newell, RTI’s director of client services for PP.

PP trading remained busy, even leaning toward robust. Spot PP prices entering August jumped by 6¢/lb. “Restricted resin production has been tightening supplies; add in rising feedstock costs, and the fledgling rally has just turned into a little bull market,” noted Greenberg. PP contracts this year were up 4¢/lb and then dropped 7¢/lb, so they are down a net 3¢ through July. This loss was generally expected to be erased in August as a price increase appeared imminent.

Unplanned PP production disruptions in June and July struck at Pinnacle, Formosa, Flint Hills, ExxonMobil, and Total, according to Newell. Both Braskem and Formosa had planned turnaround shutdowns—Braskem’s started in early August and was to last 45 days, while Formosa’s was to start this month and last 40 days. Newell expected PP availability to be somewhat constrained until all the production issues were smoothed out. He noted that strong demand in June brought demand growth for PP from -2.43% to +1.38%, relative to the average for 2013.

PS GOES HIGHER

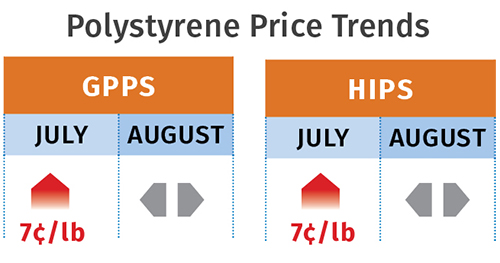

Polystyrene prices moved up a full 7¢/lb following an 80¢/gal bump in July benzene contracts.

But there was also upward pressure developing from the ethylene side, according to Mark Kallman, RTi’s v.p. of client services for engineering resins, PS, and PVC.

He expected flat-to-lower prices last month, noting that August benzene contracts settled lower by 20¢/gal. There was the problem of ethylene tightness, however, brought on by unplanned cracker shutdowns and startup delays. While July ethylene contracts had yet to be settled in early August, they were expected to move up by at least 3-4¢/lb. Still Kallman anticipated that the ethylene supply situation will have worked itself out by this month, and still saw some potential for PS prices dropping a bit.

PVC PRICES FLAT FOR NOW

PVC prices did not drop any further, remaining flat instead. The 80¢/gal July benzene contract increase and the constricted ethylene supplies brought on by unplanned production interruptions halted any further price relief, according to RTI’s Kallman.

Meanwhile, PVC suppliers had called for 2-3¢/lb increases on Aug. 1, though Kallman

expected there would be significant pushback by processors against their implementation. “I expect relief from ethylene price pressure in September and more availability of PVC as the construction season begins to slow,” he said.

Related Content

Resin Prices Still Dropping

This downward trajectory is expected to continue, primarily due to slowed demand, lower feedstock costs and adequate-to-ample supplies.

Read More

Prices for All Volume Resins Head Down at End of 2023

Flat-to-downward trajectory for at least this month.

Read More

The Fundamentals of Polyethylene – Part 1: The Basics

You would think we’d know all there is to know about a material that was commercialized 80 years ago. Not so for polyethylene. Let’s start by brushing up on the basics.

Read More

Fundamentals of Polyethylene – Part 5: Metallocenes

How the development of new catalysts—notably metallocenes—paved the way for the development of material grades never before possible.

Read MoreRead Next

Why (and What) You Need to Dry

Other than polyolefins, almost every other polymer exhibits some level of polarity and therefore can absorb a certain amount of moisture from the atmosphere. Here’s a look at some of these materials, and what needs to be done to dry them.

Read More

How Polymer Melts in Single-Screw Extruders

Understanding how polymer melts in a single-screw extruder could help you optimize your screw design to eliminate defect-causing solid polymer fragments.

Read More