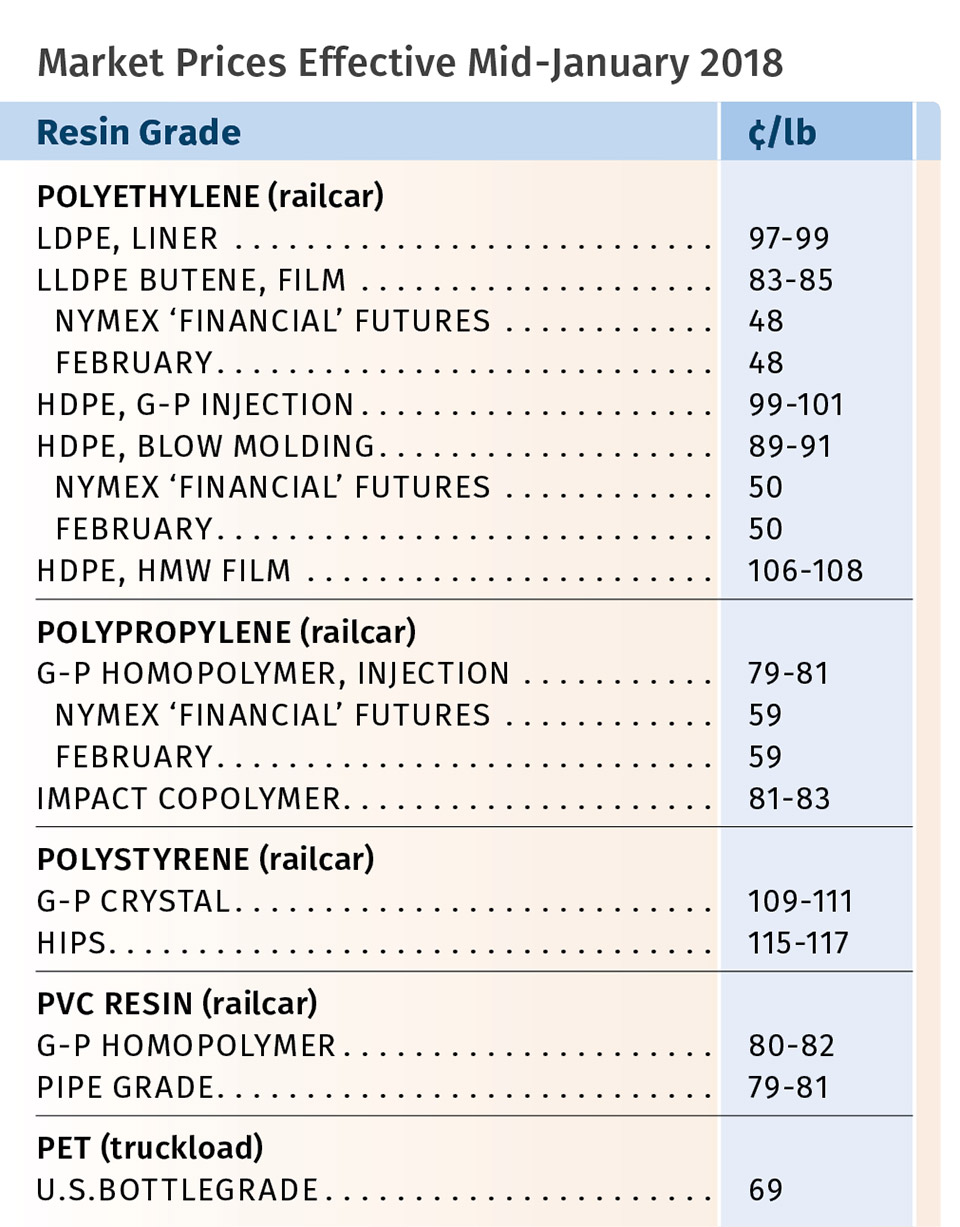

PE, PVC Prices Down; PP, PS, PET Up

But what’s going up could go down again soon.

Once again, prices of the five high-volume commodity resins were a mixed bag going into the first month of the new year. Whereas PE and PVC prices had dropped, those of PP, PS, and PET had moved up. In both cases, feedstock costs were key drivers. But the winds of change were also blowing in different directions, potentially deflating PP and PS prices while lifting PVC prices back up.

Those are the views of purchasing consultants from Resin Technology Inc. (RTi), Fort Worth, Texas; Michael Greenberg, CEO of the Plastics Exchange in Chicago; and Houston-based PetroChemWire (PCW).

PE PRICES DROP

Polyethylene prices were reported to have dropped by 3¢/lb in at least some cases in December, although suppliers announced no price reductions, according to Mike Burns, RTi’s v.p. of client services for PE. He said the price move was confirmed by several RTi clients. PCW said no suppliers had indicated a market-wide PE price reduction for December.

The Plastics Exchange’s Greenberg reported that after peaking in mid-September, spot PE prices have been sliding ever since. He noted that most spot PE prices were still several cents higher at year’s end. PCW characterized spot PE prices as mostly flat following the year-end holidays, adding that spot availability appeared scarce, and low-end December sale prices were no longer seen on the market.

RTi’s Burns, for one, ventured that further price reductions on the order of 5-7¢/lb were plausible in January and February. He noted, “If global oil prices remain up, PE suppliers will export a lot more material, which would in turn slow down domestic price reductions.” He said there are industry expectations for increased first-quarter exports, due to higher cost and lower inventories in Southeast Asia and China. Domestic PE production is pretty strong, according to Burns, who characterized first-quarter supplier inventories as “healthy but not long.”

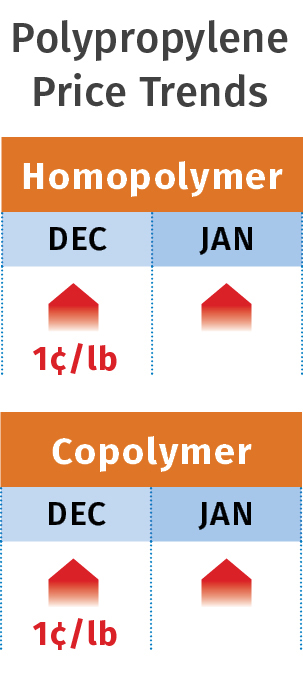

PP PRICES INCH UP, BUT REVERSAL LIKELY

Polypropylene prices moved up 1¢/lb in December as they had in November, in step with propylene monomer contracts. Scott Newell, RTi’s v.p. of PP markets, ventured that we would possibly see a bit higher PP prices in January, but he expected a reversal in the price trend to follow.

An unplanned outage at a Dow propylene unit in December had contributed to the monomer tightness, but Newell expected monomer prices to start dropping, as the new Enterprise Product Partners propylene production unit is due to be fully ramped up by now. Spot monomer prices had moved above the 50¢ mark by year’s end.

Newell noted that fourth-quarter PP production was above average, whereas demand did not bounce back as well, and he characterized the domestic market as better balanced. He expected that suppliers have been building up inventories as there are some planned PP plant shutdowns coming in the first and second quarters. He added that a significant volume of PP imports has been seen, which could dampen demand for domestic PP if prices stay up.

Both PCW and Greenberg characterized spot PP resin activity as limited. “Offers in general have been scarce, and the market has maintained an upward bias,” said Greenberg, who anticipated continued upward pressure into the new year. PCW reported spot PP prices as flat-to-higher following the holidays, with attention focused on the sharp uptick in spot propylene monomer. Despite the severe winter weather that affected the Northeastern U.S. in the first week of January, no production issues were reported for PP units at Braskem’s Markus Hook, Pa., site or that of Phillips 66 in Linden, N.J.

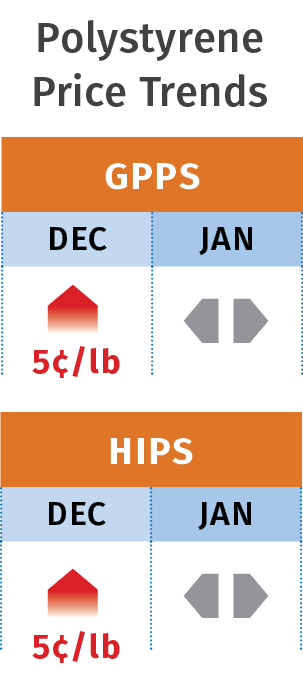

PS PRICES UP

Polystyrene prices moved up 5c/lb in December, according to PCW and Mark Kallman, RTi’s v.p. of client services for engineering resins, PS, and PVC. This was driven by a 46¢/gal increase in December benzene contracts. One PS supplier was seeking an additional 2¢/lb in January; however, January benzene contracts dropped to $3.22/gal from December’s $3.30, and spot prices last month were also dropping—an indication of improved benzene availability.

Kallman ventured that January PS prices would be flat, with the potential for a drop in prices this month, based on lower benzene prices. PCW reported that based on spot feedstock prices, the 30% ethylene/70% benzene cost formula for PS dropped back to 38.8¢/lb by the end of December, compared with 40.4¢/lb at mid-month. Kallman did add that planned styrene monomer plant shutdowns in the first quarter could hamper a PS price reduction this month.

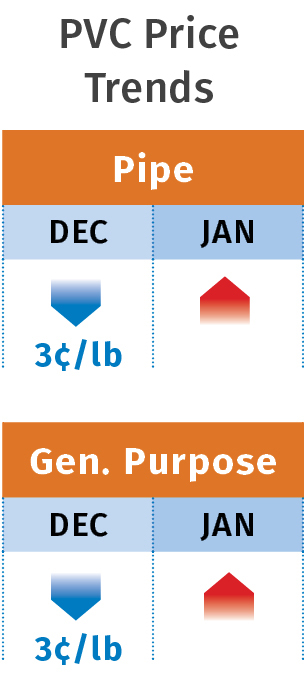

PVC PRICES DROP

PVC prices dropped in December, essentially nixing the October 3¢/lb price hike, and another 1¢ was coming off in January, according to RTi’s Kallman. On Jan. 5 PCW reported price-increase announcements for 3¢/lb effective Feb. 1 from the four major suppliers as follows:

Formosa’s applies to its PVC homopolymer suspension-grade resins and compounds; Westlake’s applies to all of its suspension grades only; increases by Shintech and OxyVinyls apply to all their PVC products.

PCW also reported that processors expected more increases to emerge in the next two months as suppliers aim to recoup the price declines of fourth-quarter 2017. According to Kallman, domestic demand dropped following the highs in November, driven by cold weather; but export demand from Southeast Asia was picking up once again and was expected to be stronger, particularly from India and China. He noted that it is generally expected that demand in the second quarter will be strong domestically and globally.

PET PRICES UP

PCW reported that domestic bottle-grade PET resin ended 2017 at 69¢/lb for Midwest spot delivery via railcar/bulk-truck shipments—which was steady from the start of December. Spot supply remained tight, as it was understood that production from M&G Chemicals’ PET plants in Apple Grove, W. Va., and Altamira, Mexico, remained at limited levels. The plants are major suppliers to U.S. customers, and both were idled in October when M&G subsidiaries filed for bankruptcy protection. The company’s unfinished “Jumbo” PET plant (80% completed) in Corpus Christie remained in limbo with no resin expected from the plant until second quarter at the earliest.

PET feedstock costs were on the rise in early 2018 due to rising global crude oil and mixed xylene (MX) prices. December North American PET feedstock costs averaged 76¢/lb, up 6.38¢/lb from November. January costs were expected to be higher than December’s, if crude-oil and paraxylene prices stayed at December levels or went higher. PCW also reported that domestic

PET prices were expected to climb over 70¢/lb in the first quarter due to less production from M&G and a drop in imports because of pending anti-dumping duties on imports from South Korea, Brazil, Indonesia, Taiwan, and Pakistan, expected to be effective March 5.

Related Content

Understanding Strain-Rate Sensitivity In Polymers

Material behavior is fundamentally determined by the equivalence of time and temperature. But that principle tends to be lost on processors and designers. Here’s some guidance.

Read More

Understanding the ‘Science’ of Color

And as with all sciences, there are fundamentals that must be considered to do color right. Here’s a helpful start.

Read More

The Effects of Temperature

The polymers we work with follow the same principles as the body: the hotter the environment becomes, the less performance we can expect.

Read More

Melt Flow Rate Testing–Part 1

Though often criticized, MFR is a very good gauge of the relative average molecular weight of the polymer. Since molecular weight (MW) is the driving force behind performance in polymers, it turns out to be a very useful number.

Read MoreRead Next

Why (and What) You Need to Dry

Other than polyolefins, almost every other polymer exhibits some level of polarity and therefore can absorb a certain amount of moisture from the atmosphere. Here’s a look at some of these materials, and what needs to be done to dry them.

Read More

Lead the Conversation, Change the Conversation

Coverage of single-use plastics can be both misleading and demoralizing. Here are 10 tips for changing the perception of the plastics industry at your company and in your community.

Read More

Troubleshooting Screw and Barrel Wear in Extrusion

Extruder screws and barrels will wear over time. If you are seeing a reduction in specific rate and higher discharge temperatures, wear is the likely culprit.

Read More