Plastics Machinery Growth Streak Still Alive In North America

Each quarter for the last 22 quarters going back to 2010, North American plastics machinery shipments have risen on a year-over-year basis.

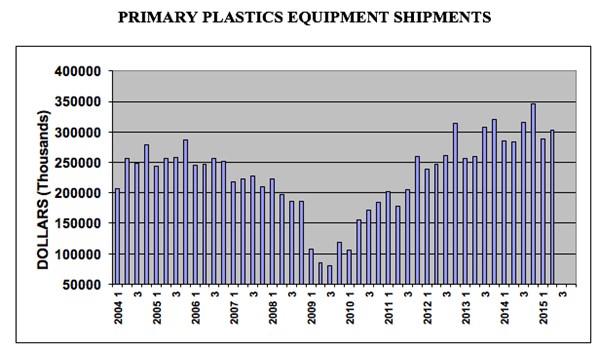

Plastics machinery sales continued an overall growth trend in the second quarter of 2015 according to SPI’s Committee on Equipment Statistics (CES), outpacing other industrial segments.

Shipments of primary plastics equipment, including injection molding, extrusion, and blow molding equipment, totaled $303.5 million in Q2 for reporting companies. This was an increase of 5.5 percent from the shipments total of $287.7 million in the first quarter, and 6.7 percent higher compared with the shipments total from the second quarter of 2014. Year to date in 2015, the value of primary plastics equipment shipments is up 3.9 percent compared to the first half of 2014.

Breakout By Technology

- Injection molding machinery shipments: Up 3.9 percent from Q2 2014

- Single-screw extruder shipments: Down 1.5 percent from Q2 2014

- Twin-screw extruder shipments: Up 1.0 percent from Q2 2014

- Blow molding machine shipments: Up 66.4 percent in Q2

- Auxiliary equipment new bookings: Up 12.4 percent in Q2

Optimistic Outlook

Although the outlook on the broader economy has been negatively impacted by concerns about China’s manufacturing sector, plastics machinery suppliers remain bullish about their market going forward according to a survey conducted by the CES.

Quoting activity was higher in the second quarter for half of the survey participants, and fully 88 percent of respondents expect conditions to either improve or hold steady in the coming quarter and during the next 12 months.

On a geographic basis, North America and Mexico were forecast to have the most promising market conditions for machinery suppliers in the coming year, according to the survey. Latin American market condition expectations are mostly steady, while the outlook for Europe and Asia are steady-to-weaker.

In terms of major end-markets, survey respondents indicated that automotive and packaging will remain strong in terms of demand for plastics products and equipment. Expectations for all other major end-markets call for firm market conditions to persist during the next 12 months.