Bouncing Back

Processors' Business Index

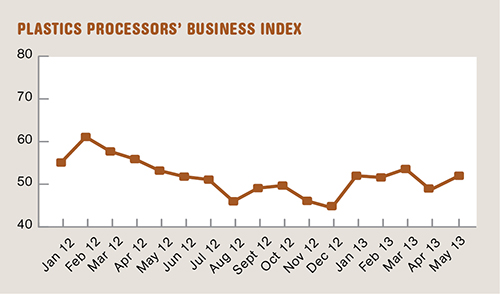

April's gain marks the fourth month out of five that the index has advanced.

.JPG;width=70;height=70;mode=crop;format=webp)

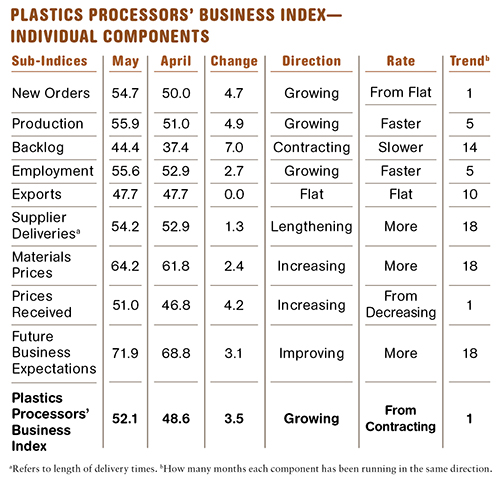

With a reading of 52.1, Gardner's Plastics Processors’ Business Index recovered from a lackluster April and showed growth for the fourth month out of the last five. Of those four months of growth, May grew at the second fastest rate.

After a flat April, new order activity recovered nicely in May. The rate of growth in production picked up significantly as well, hitting its second-fastest bump in the last five months. The same can be said for employment. Supplier deliveries lengthened more in May. Each of these four sub-indices contributed to the significant improvement in the Processors’ Business Index in May.

Another reason for the improvement in May is that the smallest facilities, those with fewer than 19 employees, showed growth for the first time since July 2012.

However, two factors are combining to keep the overall index below the levels of the first half of 2012: backlogs and exports. Backlogs, in fact, have contracted since May 2012, though they contracted at slower pace last month. (Index values under 50 indicate contraction; values over 50 indicate expansion.) Processors likely have more capacity this year because of their capital-equipment investments in 2012. So even with new orders increasing recently, processors are able to meet demand.

Exports continue to hold the overall index back, too. The dollar has been appreciating against world currencies for some time. This is putting pressure on exports. Further hurting exports is the weakness of most world economies.

Material prices continue to increase, but the good news for processors is that rate of increase was the second slowest in May over the last six months. Prices received by plastics processors for their products increased in May after decreasing in April. Processors also seemed to be more optimistic in May; future business expectations are at their second highest level since March 2012.

Both the New England and Pacific regions grew for the fourth consecutive month, with the strongest growth in New England. The East North Central region has grown for four of the last five months, while the South Atlantic region has grown in three of the last four months. The Middle Atlantic region grew in May after contracting in the previous two months. The West North Central region contracted for the second month in a row.