Processors’ Growth Returns

After a one-month dip, the market expands once more, though the rate has slowed.

.JPG;width=70;height=70;mode=crop;format=webp)

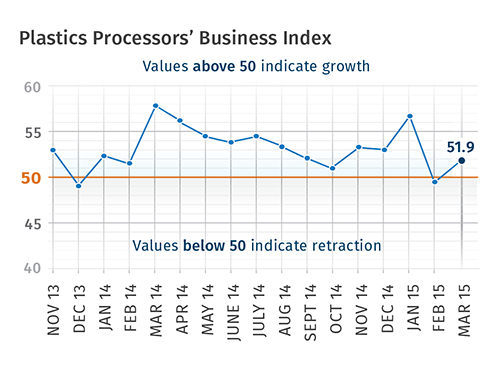

With a reading of 51.9, Gardner’s Plastics Processors’ Business Index expanded once again in March after a dip in February. Since last January, the processing market has grown every month except one. But compared with one year ago, the index actually contracted by 10.7%. This was the second straight month of such contraction. That means while the industry returned to growth, the rate of growth is noticeably slower than it was a year ago.

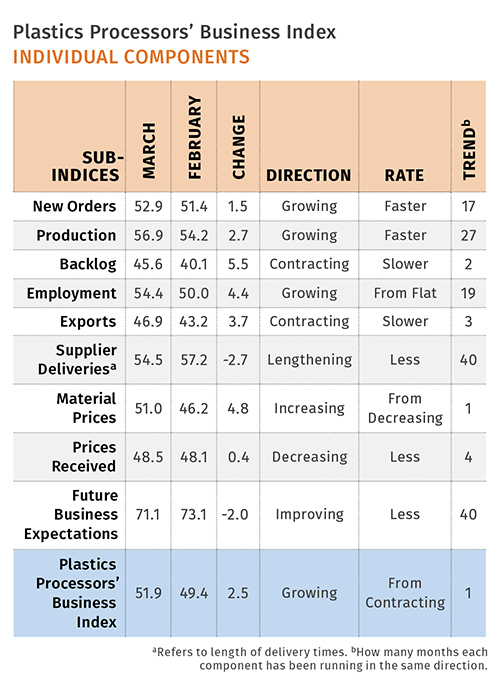

Five of the six sub-indices that are used to calculate the overall index improved in March (only supplier deliveries did not). New orders increased for the 17th straight month. Production increased for the 27th month in a row. Generally, the growth rate of production has been stronger in 2014 and 2015 than it was in 2013. Backlogs contracted for the second month in a row. March was the second month in a row that backlogs contracted by more than 14% compared with one year ago.

The trend in backlogs indicates that the growth rate of capacity utilization has likely peaked. Employment increased once again after a one-month pause in February. Exports contracted for the third consecutive month due to the relatively strong dollar. Supplier deliveries continued to lengthen at a rate consistent with the last 12 months.

Material prices increased in March after contracting in the previous two months. However, the material prices index was still well below any other point since the survey began in December 2011. Prices received by processors for their wares contracted for the third straight month. This was the longest sustained run of price decreases since the fall of 2012. Future business expectations have declined for three straight months.

In March, the index increased at every plant size. Plants with 100-249 employees had the most significant improvement, as their index increased to 56 from 52.2. Processors with 20-49 employees saw a similar increase in March and have been the fastest-growing segment in the last two months.

The West was the fastest-growing region in March after contracting last month. The North Central–East has expanded since October 2014. The Northeast grew for the third straight month.

Future capital-spending plans contracted month-over-month for the eighth time in nine months. The rate of contraction has been quite strong in three of the last four months. The annual rate of change has contracted at an accelerating rate for six straight months and was in double digits in March.

Related Content

-

Plastics Processing Contracted Again in March

Processing activity contracted for the ninth straight month, and at a faster rate.

-

Processing Slips as Summer Simmers

Monthly index suggests slower growth in June for plastics processors overall and contraction for custom firms.

-

Plastics Processing Activity Near Flat in February

The month proved to not be all dark, cold, and gloomy after all, at least when it comes to processing activity.