Growth Continues, Slowly

Processing market grows for the 11th month out of 12.

.JPG;width=70;height=70;mode=crop;format=webp)

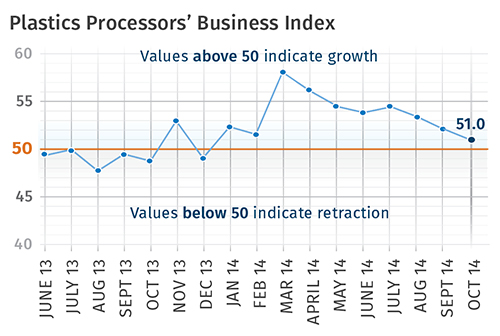

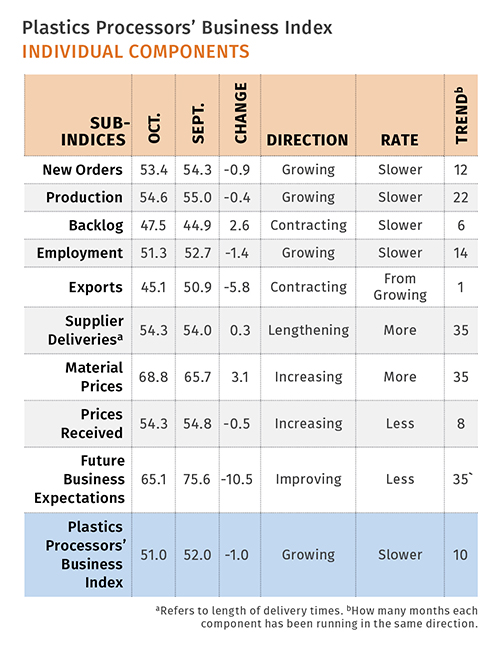

With a reading of 51 in October, Gardner Business Media’s Plastics Processors’ Business Index showed growth for the 11th time in 12 months. Yet the index was at its lowest level since December 2013, the last time it contracted. The processing market has seen slower growth since its peak in March. But compared with October ’13, the index was up 4.5%. The annual rate of change has accelerated every month in 2014, reaching 8% in October.

New orders have grown for 12 straight months, though the rate of growth decelerated to its slowest pace since February. Production expanded at a similar rate, but was at its lowest level of the year in October.

Backlogs have contracted for six months in a row, but the index was at its highest level since July. Compared with a year ago, the backlog index increased 12.8% in October. This was the second time in three months that the month-over-month rate of growth was above 10%. The annual rate of change in backlogs continued to grow at an accelerating rate, which indicates that capacity utilization among processors should increase in 2015.

After increasing last month, exports contracted at their fastest rate since December 2013. Supplier deliveries have lengthened at a consistent rate in 2014.

Material prices have increased at an accelerating rate since August. Fortunately for processors, the prices they received for their products continued to increase at a significant rate. Future business expectations had their largest drop in the history of the index in October.

Facilities with more than 250 employees failed to grow for the first time in 2014. Processors with 100-249 employees continued to grow at a strong rate. Plants with 50-99 employees contracted for the second time in the last three months. After contracting last month, business for processors with 20-49 employees expanded. Processors with 1-19 employees contracted for the fifth month in a row.

The North Central–East region expanded at its fastest rate since July. The Southeast region has expanded since July 2013.

Capital-spending plans were at their lowest level since October 2012. They fell 30.2% compared with last October. This was the second month in a row that spending plans contracted by more than 30% month over month. The annual rate of change contracted for the first time since the index began in December 2011.

Related Content

-

How Much L/D Do You Really Need?

Just like selecting the extruder size and drive combination, the L/D should be carefully evaluated.

-

How to Estimate and Control Head Pressure

You rightfully worry about melt temperature, but don’t overlook head pressure, because the two are closely linked and will influence line performance.

-

Troubleshooting Screw and Barrel Wear in Extrusion

Extruder screws and barrels will wear over time. If you are seeing a reduction in specific rate and higher discharge temperatures, wear is the likely culprit.