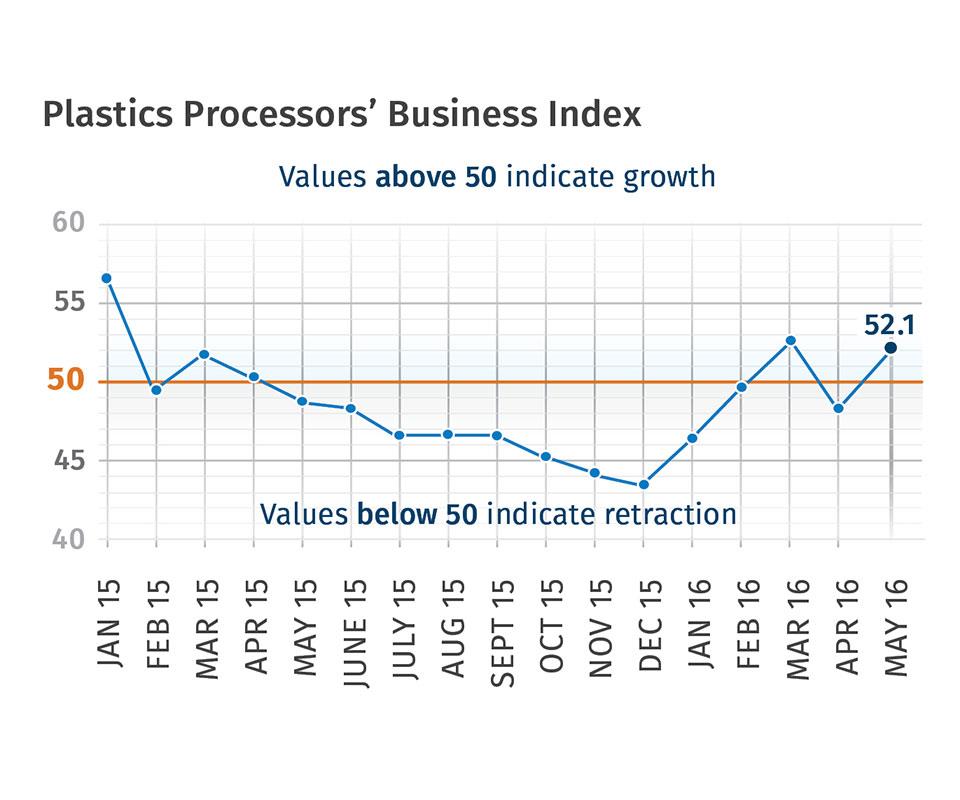

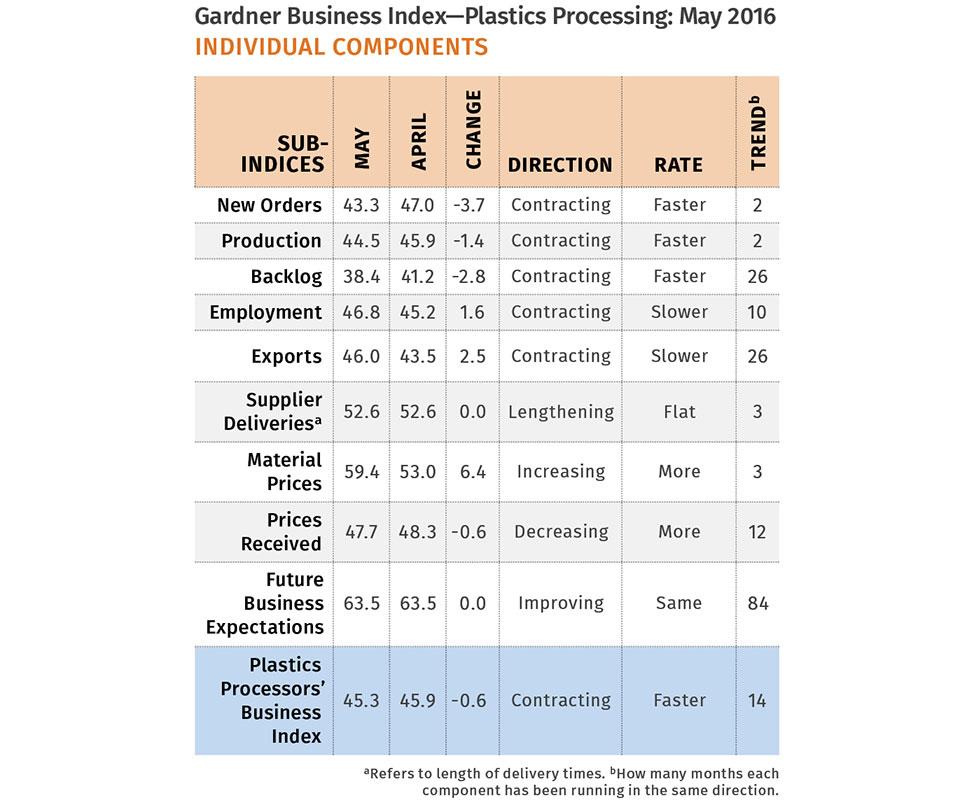

May’s Index: 52.1

Large and mid-sized processors doing particularly well.

.JPG;width=70;height=70;mode=crop;format=webp)

With a reading of 52.1, Gardner’s Plastics Processing Business Index grew for the second month out of three in May. The index reveals that the industry has improved significantly since December 2015.

New orders increased for the third time in four months; they have been surging in 2016 compared with the second half of 2015. Production has expanded in three of the last four months too. While the backlog index contracted for the 16th month in a row, the index has been at virtually the same level for four months. Employment increased for the fourth time in five months. The export index contracted at a significantly slower rate in May. The index was at its highest level since December 2014, which was the last time exports did not contract. Supplier deliveries lengthened for the fourth month in a row.

Material prices increased for the second month in a row. Prices received increased for the first time since November 2014. Future business expectations improved from last month, reaching their second-highest level since April 2015.

The improvement in the industry in May was led by larger facilities. Processors with more than 250 employees grew for the fourth month in a row. Their index in May was the only time it has ever been above 60. Plants with more than 100-249 employees expanded for third month in a row. Facilities with 50-99 employees expanded for the sixth in a row, also recording an index above 60. Companies with 20-49 employees contracted for the second month in a row. The index at processors with 1-19 employees contracted, as it has since February 2015.

The fastest-growing region in May was the Southeast. It has grown four of the last five months. The Northeast grew at a strong rate in May and for the fourth month in a row. The South Central grew for the second time in four months. And, the North Central-East grew at a minimal rate in May but for the third time in four months. Both the North Central-West and West contracted for the second month in a row.

Future capital spending plans jumped above $1 million per plant for the second month in a row. Compared with one year ago, future capital spending plans increased more than 46%. This was the third time in four months that spending plans increased compared with one year ago. Capital equipment spending in the plastics industry seems to be entering its next up cycle.

ABOUT THE AUTHOR

Steven Kline Jr. is part of the fourth-generation ownership team of Cincinnati-based Gardner Business Media, which is the publisher of Plastics Technology. He is currently the company’s director of market intelligence. Contact: (513) 527-8800 email:skline2@gardnerweb.com blog: gardnerweb.com/economics/blog

Related Content

-

Make Every Shot Count: Mold Simulation Maximizes Functional Parts From Printed Tooling

If a printed tool only has a finite number of shots in it, why waste any of them on process development?

-

Additive Fusion Technology Optimizes Composite Structures for Demanding Applications

9T Labs continues to enhance the efficiency of its technology, which produces composite parts with intentionally oriented fibers.

-

Large-Format “Cold” 3D Printing With Polypropylene and Polyethylene

Israeli startup Largix has developed a production solution that can 3D print PP and PE without melting them. Its first test? Custom tanks for chemical storage.