Processing Market Flattens

Processing has grown significantly since the beginning of 2014, but April dipped 11% on a year-to-year basis.

.JPG;width=70;height=70;mode=crop;format=webp)

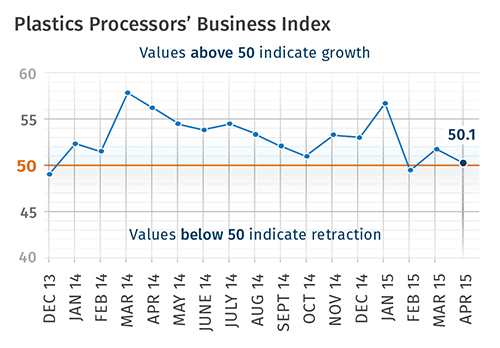

With a reading of 50.1, Gardner’s Plastics Processor’s Business Index was virtually flat in April. In fact, over the last three months, conditions in the industry have been largely unchanged. This is not all bad, considering that processing has grown significantly since the beginning of 2014. But compared with one year ago, April’s index contracted by 11%. That was the fastest rate of contraction since April 2013.

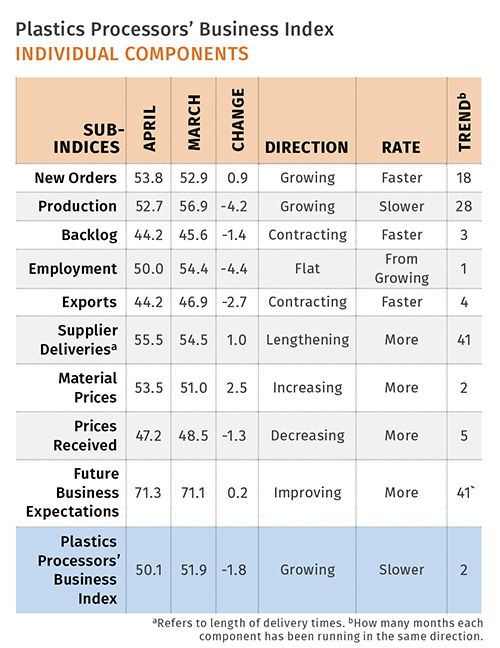

New orders increased for the 18th month in a row; the rate of increase has accelerated in each of the last two months. Production expanded for the 28th consecutive month. But this index was at its lowest level since December 2013. Backlogs contracted for the third straight month. Compared with a year ago, the backlog index has contracted at slightly more than 14% for three months in a row. This indicates that capacity utilization has seen its peak rate of growth in this cycle.

For the second month in three, employment was unchanged. Hiring in 2015 has clearly slowed below the rate of 2014. Exports continued to contract due to the relatively strong dollar. The export index has trended down since its peak in May 2014.

After contracting in the first two months of the year, materials prices have increased in the last two months. However, the rate of increase was still below the previous slowest rate of increase in material prices. Prices received have contracted at a slightly accelerating rate for five straight months. Future business expectations leveled off after falling in the previous four months.

Facilities with 100-249 employees recorded improved business conditions in April. In fact, these companies grew at their second fastest rate since September 2014. All other plant sizes saw a decline in business. Plants with 20-99 employees grew at a marginal rate in April. Processors with 1-19 employees contracted for the fourth month in a row.

Almost every region switched from growth to contraction or from contraction to growth. The North Central-West region was the fastest-growing region after contracting last month.

Future capital-spending plans have been hit hard in the last three months. They have contracted for seven straight months, and the rate of contraction has accelerated in the last three months. In April, future spending plans contracted 45.5% versus a year ago. The annual rate of change has contracted at an accelerating rate for seven months.

Related Content

-

Plastics Processing Activity Near Flat in February

The month proved to not be all dark, cold, and gloomy after all, at least when it comes to processing activity.

-

Plastics Processing Growth Slows Slightly

May reading for plastics processors is, for the most part, a continuation of what we saw in April.

-

Plastics Processing Contraction Continues

Contraction dominated the GBI index for overall plastics processing activity and almost all components, collectively suggesting a slowdown.