Second Contraction in Three Months

Slowdown among small-to-mid-size processors drags index down.

.JPG;width=70;height=70;mode=crop;format=webp)

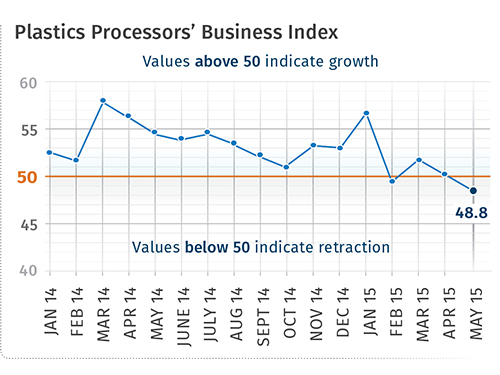

With a reading of 48.8 in May, Gardner’s Plastics Processors’ Business Index contracted for the second time in three months. May’s index was the lowest since August 2013. Between then and now, the plastics processing business showed strong month-on-month growth. But compared with one year ago, the index has contracted more than 10% for three months in a row. On an annual basis, the processing industry was still growing in May, but there were some signs of softening in the recent data.

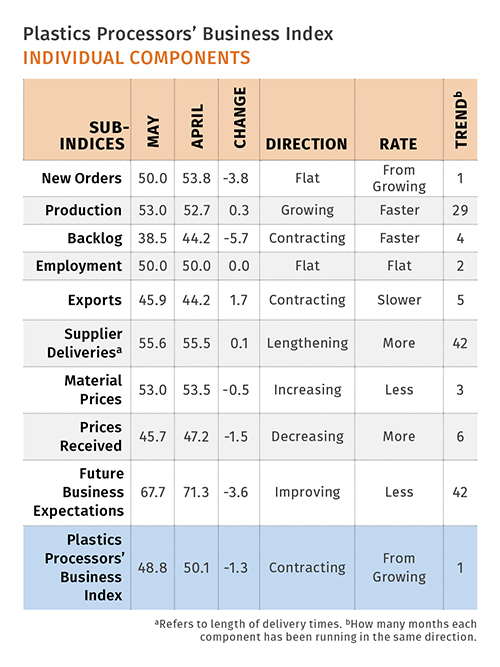

New orders were unchanged in May, ending a streak of 18 straight months of growth. Other than a significant spike in new orders in January, the new orders index has trended down steadily since March 2014. Production continued to expand, but for the second month in a row the index level was the lowest since December 2013. Because production has remained much stronger than new orders, the backlog index has tanked.

In May, the backlog index was at its lowest level since April 2013. The trend in backlogs indicates that capacity utilization will weaken for the rest of 2015.

Employment was unchanged for the third time in four months. Exports continued to contract, but the index has started to trend upward the last four months.

Material prices have increased for the last three months, as the price of oil has risen somewhat. However, the material prices index was still lower than at any other time since this survey began in December 2011. The index of prices received has fallen noticeably since October 2014. In May, prices received decreased at their fastest rate since the survey began. The future business expectations index has steadily declined since December 2014.

Processors with 100-249 employees continued to see improving business conditions in May. Their index has been above 55 for five of the last six months. Companies with 50-99 employees contracted for the first time in 2015. Processors with 20-49 employees contracted for the first time since September 2014, dragging the overall index down in May.

The Southeast was easily the fastest-growing region in May. It has grown for two straight months. The Northeast contracted after having grown for the previous four months.

Future capital spending plans were hit hard. They have been below average for four straight months. In those four months they have contracted at least 21% compared with a year ago.

Related Content

-

New Tool Steel Qualified for Additive Manufactured Molds and Dies

Next Chapter Manufacturing says HTC-45 — an optimized H-13 — will offer superior thermal transfer and longer tool life.

-

Business Slowing? There's Still Plenty of Stuff to Do

There are things you may have put off when you were occupied with shipping parts to customers. Maybe it’s time to put some of them on the front burner.

-

3D Printing of Injection Molds Flows in a New Direction

Hybrids of additive manufacturing and CNC machining can shorten tooling turnaround times.