Surging Growth

Processors have been expanding at a fast and furious pace since October.

.JPG;width=70;height=70;mode=crop;format=webp)

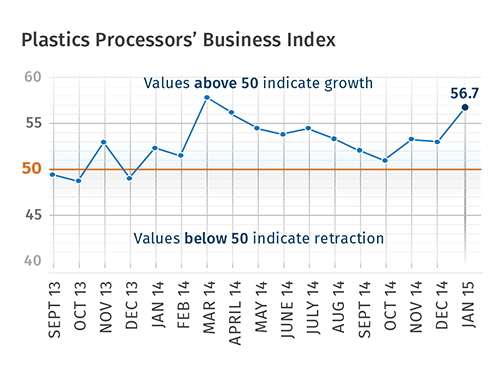

With a reading of 56.7 in January, Gardner’s Plastics Processors’ Business Index showed growth for the 14th time in 15 months. Thanks to falling oil prices, plastics processors have been expanding at a furious pace since last October. In fact, the index reached its second highest level since March 2012. Compared with a year ago, the index increased 8.4% for the second month in a row. The annual rate of growth accelerated for the first time since October.

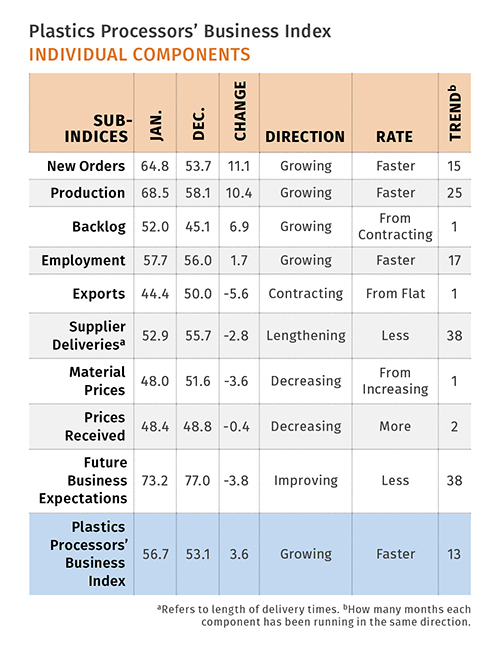

New orders have grown for 15 consecutive months and expanded at their fastest rate since we started the index in December 2011. Production also expanded rapidly in recent months. The production index was at its highest level ever in January.

Backlogs expanded for the first time since last April. Compared with one year ago, backlogs increased 11.6%. This trend indicates that there should be accelerating growth in capacity utilization into the second quarter of this year. This should lead to strong capital spending throughout 2015. The employment index also has increased significantly since October. Supplier deliveries were lengthening at their slowest rate since January 2014.

Thanks to the dramatic decrease in oil prices since last June, material prices contracted for the first time in the history of the index. The index has fallen sharply since October. Prices received contracted slightly for the second month in a row. This is the first significant contraction in prices received since April 2013. While future business expectations fell somewhat from last month, they remain at a relatively high historical level.

The four plant sizes we track that have more than 20 employees all recorded an index above 60 in January. That indicates a fairly widespread expansion across the industry. However, the smallest processors, those with fewer than 20 employees, contracted once again. These small processors have expanded in just two months since March 2014.

Every region expanded in January. The fastest growing region was the Southeast and it was closely followed by the North Central–East. Both regions had an index above 60. The North Central–West also expanded at a significant rate.

Future capital-spending plans hit their second highest level in the last five months. Compared with a year ago, they were down just 0.2%. The annual rate of change has contracted at an accelerating rate for four straight months.

Related Content

-

At NPE, Cypet to Show Latest Achievements in Large PET Containers

Maker of one-stage ISBM machines will show off new sizes and styles of handled and stackable PET containers, including novel interlocking products.

-

50 Years of Headlines … Almost

I was lucky to get an early look at many of the past half-century’s exciting developments in plastics. Here’s a selection.

-

How Was K 2022 for Blow Molding?

Over a dozen companies emphasized sustainability with use of foam and recycle, lightweighting and energy savings, along with new capabilities in controls, automation and quick changeovers.