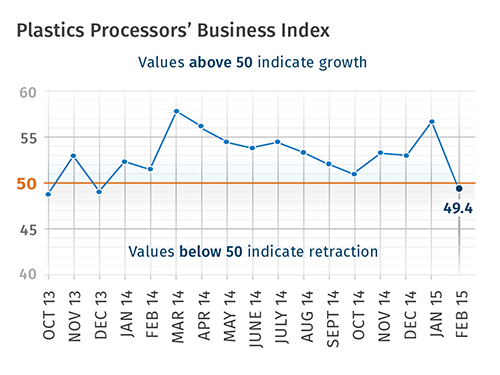

First Contraction Since December 2013

A temporary pause after 15 straight months of expansion?

.JPG;width=70;height=70;mode=crop;format=webp)

With a reading of 49.4, Gardner’s Plastics Processors’ Business Index contracted in February for the first time in more than a year. The dip was extremely moderate and it could be just a hiccup in the processing sector’s expansion after a rapid acceleration in growth since October 2014. Compared with February 2014, the index contracted on a year-to-year basis for the first time since October 2013. But the annual rate of change was still growing at a significant rate.

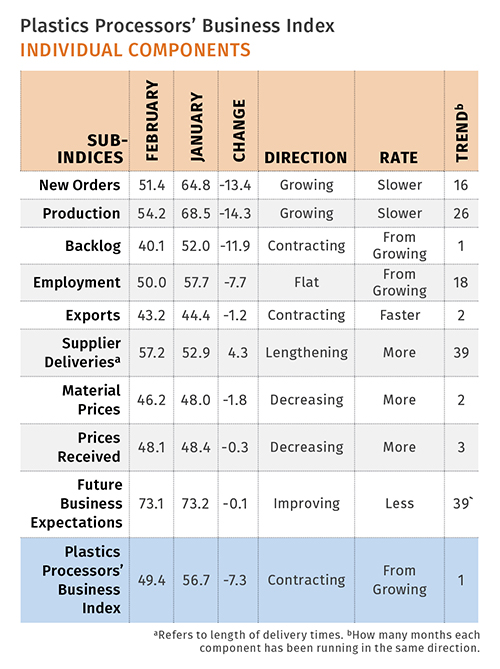

The overall index slipped due to significant declines in the indices for new orders, production, and backlogs. However, new orders expanded for the 16th straight month, while production expanded for the 26th month in a row.

The backlog index in February was at its lowest level since April 2013. February was the first month-over-month contraction in backlogs since October 2013. The annual rate of change, however, was still growing at a significant rate.

Meanwhile, employment dipped for the first time since August 2013. Exports contracted at their fastest rate since August 2012, due to significant strengthening in the dollar relative to other currencies. Supplier deliveries lengthened at their fastest rate since May 2012.

Material prices declined for the second month in a row, largely as a result of the steep fall in oil prices. Oil prices have stabilized recently. Prices received by processors declined for the third straight month. Future business expectations declined slightly from last month but remain at a good level.

In February, the rate of growth at larger facilities cooled sharply. Plants with 100-249 employees had their second lowest index in the last year. Plants with 50-99 employees were flat in February. Facilities with 20-49 employees expanded at a slower rate than last month, too. However, their index was above 55 for the fifth straight month.

Facilities with fewer than 20 employees contracted for the second month in a row.

The significant decline in business conditions was due to drops in the North Central–East and Southeast regions. The fastest-growing region was the North Central–West. The Northeast grew for the second month in a row. The West contracted slightly.

Future capital-spending plans contracted month-over-month for the seventh time in eight months. The annual rate of change has contracted at an accelerating rate for five months in a row.

ABOUT THE AUTHOR: STEVE KLINE JR.

Steven Kline Jr. is part of the fourth-generation ownership team of Cincinnati-based Gardner Business Media, which is the publisher of Plastics Technology. He is currently the company’s director of market intelligence. Contact: (513) 527-8800;

email: skline2@gardnerweb.com; blog: gardnerweb.com/economics/blog

Related Content

-

Upgraded Former is Faster, More Precise

New features reportedly offer more efficient production of trays, containers, hinged boxes, pallets, blisters, lids and technical products.

-

Interactive Training for Injection, Extrusion and Other Processes

Paulson has four in-booth stations demonstrating its various training solutions.

-

Manufacturer Helps Clean Up Global Waterways with Reclaimed Plastics

RSP and Oceanworks partnership diverts plastic wastes from waterways for incorporation into new products.