Industry Expands Again

January was the third month in a row and the fifth time in six months that index was higher than it was one year ago.

.JPG;width=70;height=70;mode=crop;format=webp)

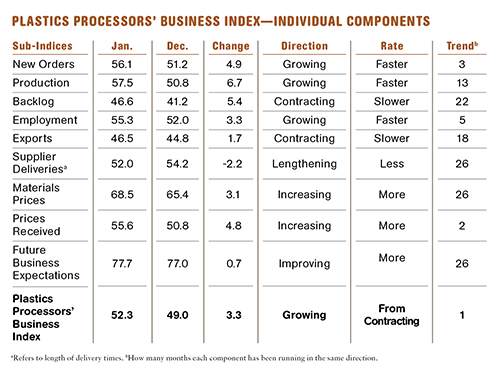

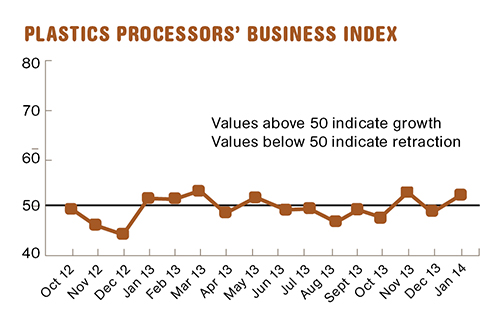

With a reading of 52.3, Gardner’s Plastics Processors’ Business Index showed that the market grew for the second time in three months. The level of business activity has been picking up since last August. The rate of growth in January was the third fastest since May 2012. Compared with one year ago, the index was up 1.4%. January was the third month in a row and the fifth time in six months that index was higher than it was one year ago.

New orders increased for the third straight month. The rate of growth in new orders was the fastest since March 2013. The rate of growth in production jumped significantly in January after slowing noticeably in December. Production is expanding at the second fastest rate since May 2012.

Backlogs continue to contract, though. Since December 2012 the rate of contraction in backlogs has slowed. This suggests that there could be some modest improvement in capacity utilization in 2014. Exports contracted at roughly the same rate they have since the summer of 2012. Supplier deliveries are still lengthening, but doing so at one of the slowest rates in the survey’s history.

Material prices had been increasing at a slower rate throughout most of 2013. But over the last two months, they have increased at a significantly faster clip. Prices received are increasing at a faster rate as well, though far below that of material prices. Future business expectations are noticeably higher than they were throughout 2013. In fact, future business expectations are their second highest level since the index began in December 2011.

Larger processors are still performing better than smaller ones. Facilities with more than 50 employees generally saw better business conditions in January. These plants have grown in three of the last four months. Smaller processors are doing better than they did in most of 2013, but are still lagging the larger processors. Facilities with 20-49 employees have grown two of the last three months, but the rate of growth has been barely positive. Facilities with fewer than 20 employees continue to contract, but their index is at the second highest level since July 2012.

After two months of contraction, the New England region expanded at the fastest rate in January. Its rate of growth in January was the fastest of any region in any month in the history of this index. The West North Central region had the second fastest rate of growth and grew for the second time in three months.

Future capital spending plans increased 4.8% compared with last year. This was after the one-month rate of change contracted in December for the first time in survey’s history. It appears that future capital spending plans are slowing down slightly. But, if the overall trend in the industry continues to be up, then future spending plans should turn back around soon.

ABOUT THE AUTHOR

Steven Kline Jr. is part of the fourth-generation ownership team of Cincinnati-based Gardner Business Media, which is the publisher of Plastics Technology. He is currently the company’s director of market intelligence. Contact: (513) 527-8800; email: skline2@gardnerweb.com; blog: gardnerweb.com/economics/blog.

Related Content

How to Extrusion Blow Mold PHA/PLA Blends

You need to pay attention to the inherent characteristics of biopolymers PHA/PLA materials when setting process parameters to realize better and more consistent outcomes.

Read More

Best Methods of Molding Undercuts

Producing plastics parts with undercuts presents distinct challenges for molders.

Read More

Consistent Shots for Consistent Shots

An integral supplier in the effort to fast-track COVID-19 vaccine deployment, Retractable Technologies turned to Arburg and its PressurePilot technology to help deliver more than 500 million syringes during the pandemic.

Read More

US Merchants Makes its Mark in Injection Molding

In less than a decade in injection molding, US Merchants has acquired hundreds of machines spread across facilities in California, Texas, Virginia and Arizona, with even more growth coming.

Read MoreRead Next

For PLASTICS' CEO Seaholm, NPE to Shine Light on Sustainability Successes

With advocacy, communication and sustainability as three main pillars, Seaholm leads a trade association to NPE that ‘is more active today than we have ever been.’

Read More

Lead the Conversation, Change the Conversation

Coverage of single-use plastics can be both misleading and demoralizing. Here are 10 tips for changing the perception of the plastics industry at your company and in your community.

Read More

Beyond Prototypes: 8 Ways the Plastics Industry Is Using 3D Printing

Plastics processors are finding applications for 3D printing around the plant and across the supply chain. Here are 8 examples to look for at NPE2024.

Read More