Price Relief Continues in Commodity Resins

Resin Buying Strategies

Further price erosion is projected for at least this month, particularly in the case of polyolefins and polystyrene.

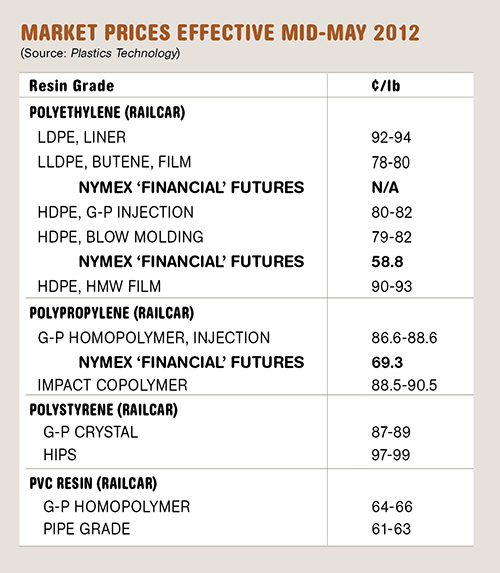

Prices of the four commodity thermoplastics were flat or lower last month. Key driving factors include rapidly declining feedstock prices, lackluster domestic demand, sluggish exports, and suppliers’ mounting resin inventories. Further price erosion is projected for at least this month, particularly in the case of polyolefins and polystyrene, according to consultants from Resin Technology Inc. (RTi), Fort Worth, Tex. , and CEO Michael Greenberg of The Plastics Exchange in Chicago.

PE PRICES SLIPPING

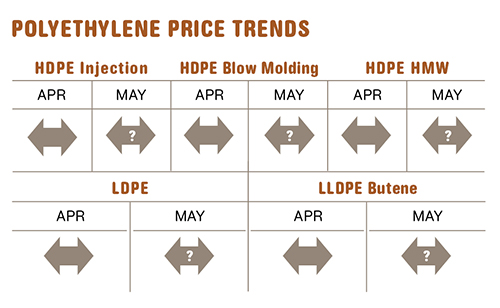

Contract polyethylene prices were flat in April, following increases totaling 6¢/lb between February and March. However, price reductions of 4¢ to 6¢ were expected to be in place by the end of last month, according to both Mike Burns, v.p. of PE at RTi, and Greenberg of The Plastics Exchange. Further price drops were projected for June.

These developments were in step with lower PE spot prices, which dropped a total of 6¢/lb within a 30-day period, according to Greenberg. As key contributing factors he cites the lowest domestic demand in two years combined with the lowest export activity since January 2009.

In addition, PE plants were still operating at over 90% of capacity during April, with suppliers’ inventories accumulating 700 million lb so far this year, according to Greenberg.

Last, but not least, ethylene monomer prices have been dropping rapidly as planned maintenance outages came to a close last month, and further price reductions were expected. Spot ethylene prices for May delivery dropped from a high of 75¢/lb to 54.25¢/lb. Ethylene for third-quarter delivery last traded at around 51.5¢, with fourth-quarter material another 2-3¢ lower, according to Greenberg.

PP PRICES BOTTOMING OUT

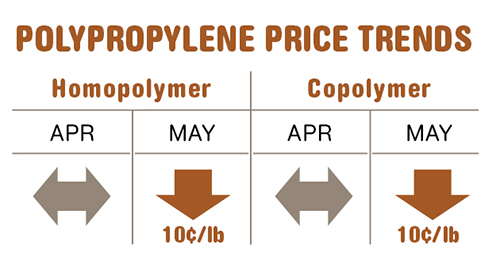

Contract prices for both polypropylene resin and propylene monomer were flat in April, though spot PP continued to sell at heavy discounts. Both monomer prices and PP contract prices dropped by 10¢/lb in May.

A bit more price erosion is likely this month, after which prices will have bottomed out, according to Scott Newell, director of client services for PP at RTi.

PP demand in both March and April were very poor, with suppliers’ inventories continuing to grow by around 50 million lb. Says Newell, “This has been a weak market but we expect to see some rebound, most likely starting this month.” He also noted that planned cracker outages would come to completion by the end of May, so that monomer availability is expected to improve.

Greenberg of The Plastics Exchange sees the current PP market as oversupplied. He points out that even though monomer contract prices dropped by a dime to 67.5¢/lb, followed by PP contract prices, spot prices for both monomer and resin remained at a sharp discount to contract prices through mid-May.

For example, spot monomer at mid-month traded in the low 50¢/lb range and spot PP was in the upper 60s. Another significant price reduction in both monomer and resin is likely this month, with the forward market flattening out after that, according to Greenberg.

PS PRICES MOVING SOUTH

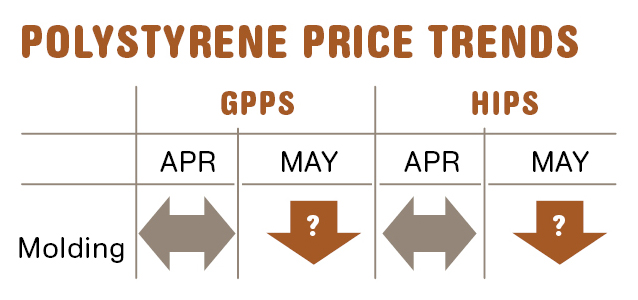

Polystyrene prices peaked in early April and stayed there through last month. Price hikes for May 1 of 2¢/lb issued by Styrolution and Total and 4¢/lb by Americas Styrenics appeared to have no momentum by mid-month, as feedstock prices slumped. Based on this movement and weak demand, GPPS and HIPS prices are projected to drop this month.

Spot benzene prices fell by more than 10¢/gal, spot ethylene prices dropped 25%. Both spot and contract styrene monomer prices remained relatively flat from February through May, despite weak demand. Spot feedstock prices were dropping, however, and are likely to continue that trajectory, which will ultimately bring down the cost of the monomer, according to Stacy Shelly, RTi’s director of business development for engineering resins, PS, and PVC.

Meanwhile, the average settlement for May butadiene contracts dropped 7¢/lb from April to $1.48/lb. Spot butadiene pricing has declined for six consecutive weeks.

Ditto for global butadiene prices, as demand is weak and inventories are ample. Shelly sees further reductions, noting: “The HIPS premium over GPPS should then begin to narrow.”

PVC PRICES FLAT TO DOWN

PVC resin prices were flat through April, as ethylene contract prices settled lower by 0.5¢/lb, and a further decline was expected for May by Mark Kallman, RTi director of client services for engineering resins and PVC.

PVC resin demand in 2012 has been steady, with domestic demand up and exports down. Domestic demand in January and February was spurred by the unusually warm winter and then flattened out by April.

Meanwhile, resin production rates, which had been throttled back to the low-to-mid 70% range earlier in the year, were moving back up.

April production rates were in the upper 80s, and suppliers’ inventories were building, according to Kallman. PVC pricing for now is expected to be flat to lower.

Related Content

Density & Molecular Weight in Polyethylene

This so-called 'commodity' material is actually quite complex, making selecting the right type a challenge.

Read More

Prices for All Volume Resins Head Down at End of 2023

Flat-to-downward trajectory for at least this month.

Read More

Resin Prices Still Dropping

This downward trajectory is expected to continue, primarily due to slowed demand, lower feedstock costs and adequate-to-ample supplies.

Read More

Fundamentals of Polyethylene – Part 5: Metallocenes

How the development of new catalysts—notably metallocenes—paved the way for the development of material grades never before possible.

Read MoreRead Next

Troubleshooting Screw and Barrel Wear in Extrusion

Extruder screws and barrels will wear over time. If you are seeing a reduction in specific rate and higher discharge temperatures, wear is the likely culprit.

Read More

Advanced Recycling: Beyond Pyrolysis

Consumer-product brand owners increasingly see advanced chemical recycling as a necessary complement to mechanical recycling if they are to meet ambitious goals for a circular economy in the next decade. Dozens of technology providers are developing new technologies to overcome the limitations of existing pyrolysis methods and to commercialize various alternative approaches to chemical recycling of plastics.

Read More