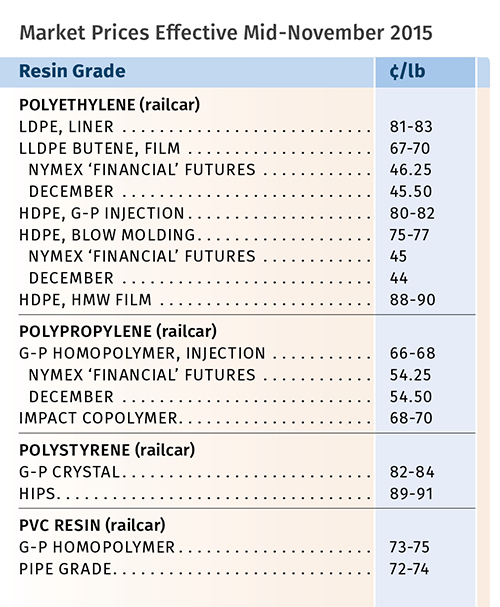

Commodity Resin Prices Flat or Lower

Mostly quiet forecast for the end of the year.

Prices for PE and PS remained flat in October, while PVC prices dropped, and PP tabs saw a modest increase. The last two months of 2015 were expected to see flat pricing, with the exception of PVC, which was likely to drop a bit farther. This was despite the fact that PE suppliers were aiming for an increase, and PP producers were looking to implement more margin increases. That was the outlook of purchasing consultants at Resin Technology, Inc. (RTi) of Fort Worth, Texas, and CEO Michael Greenberg of The Plastics Exchange in Chicago. This report explores their views in more detail, supported by comments from IHS Chemical and PetroChem Wire, both in Houston.

PE PRICES HOLDING

Polyethylene prices in October PE were stable, with most processors having restocked in September. A pending 5¢/lb increase for Nov. 1 did not appear to have a chance of implementation. In fact, industry sources expected PE prices to remain flat through year’s end.

Mike Burns, v.p. of client services for PE at RTi, did not see current market drivers supporting an increase: “We are at a good balance of supply and demand, with adequate exports and limited finished-goods imports. We would lose that balance if prices increased. I don’t think suppliers have the strength to push this one through.” He projected that prices will remain stable until oil prices approach $60/bbl, noting that current forecasts for crude oil in 2016 are in the $50-59 range.

Nick Vafiadis, IHS’s global business director for plastics and polyolefins, sees domestic PE demand up 3.1% and exports up 8.7%, for a total increase of 4.5% through September.

Greenberg noted that the PE spot market was very active in October’s last two weeks, with prices 2¢lb higher for most grades of generic prime and offgrade. RTi’s Burns conceded that spot prices were firming and not expected to go lower in November or December. One factor was that spot ethylene monomer prices were holding steady and likely to increase, as prebuying was expected prior to scheduled cracker turnarounds in the first and second quarters of 2016.

PetroChem Wire reported that restocking coupled with planned and unplanned PE production outages appeared to tighten availability, with spot prices being pushed higher as a result.

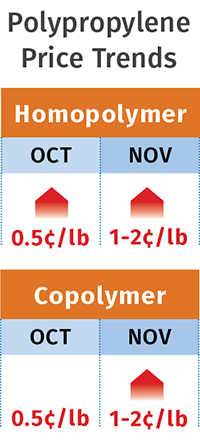

PP PRICES UP SLIGHTLY

Polypropylene prices in October went up 0.5¢/lb, in step with the half-cent increase in propylene monomer contracts. Noted Greenberg, “October monomer contracts settled at 30.5¢/lb. Aside from the 1¢/lb February increase, this modest gain was the first since October 2014, which incidentally was the market high at 76.5¢/lb.” He ventured that November monomer contracts would see another very modest increase.

Meanwhile, PP suppliers were intent on implementing further margin increases. RTi’s director of client services for PP, Scott Newell, noted that suppliers announced margin increases of 6¢/lb in October, but most pushed off implementation to Nov. 1, and one supplier split the raise in half for November and December. PP prices actually dropped a total of about 18¢/lb through the third quarter of this year, but suppliers managed to squeeze out 13-14¢/lb of margin expansion in that same time frame. The new 6¢/lb being sought would bring the total margin expansion to 19-20¢/lb. It would end the year with PP prices reversing their downward course for a 1-2¢/lb hike.

“Availability is a key issue,” said Newell. “Resin imports are becoming a threat little by little, and domestic processors are interested, but this is a slow process as there are issues such as how the material is shipped and handled and the need to test incoming material. As we come to the end of the year, domestic demand appears to be roughly 6% higher, which is pretty impressive, and supply is tightly balanced.”

PetroChem Wire noted at end of October that there were reports of increased PP shipments from Asian manufacturers to the West Coast. It also reported that contract discussions for 2016 were ongoing, with suppliers eyeing further margin increases next year and end users looking to diversify their supply base across domestic and international sources.

Joel Morales, IHS’s director of polyolefins for North America, confirms that imports are increasing and pose challenges ranging from long lead times to material-handling and quality issues. “Until 2019, when new domestic PP capacity comes on stream, we will continue to see imports of PP pellets and finished goods,” he said.

Greenberg noted that “well-priced PP imports are working their way beyond the coasts, as some processors in need of material are grudgingly willing to rip 25-kg bags to get supplies.”

Greenberg also noted increased spot trading and growing concerns over material availability. “As processors begin to look towards year-end, some have begun to sell off unneeded material. Several million pounds of prime and offgrade PP has been made available in different locations, enhancing liquidity in this otherwise tightly supplied market.”

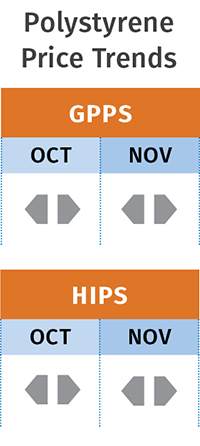

PS PRICES FLAT

Polystyrene prices were flat in October and looked to stay that way last month, according to Mark Kallman, RTi’s v.p. of client services for engineering resins, PS, and PVC. This was after PS tabs fell a total of 12¢/lb in August and September, following steep drops in the price of benzene and lower ethylene contract prices.

October benzene contracts moved up a modest 6¢/gal—a negligible amount to have any effect on PS prices, while September ethylene contracts dropped another penny to 28.5¢/lb—the lowest since 2008. Continued price competition among suppliers, coupled with a seasonal slowdown in demand, was likely to keep PS prices flat this month as well.

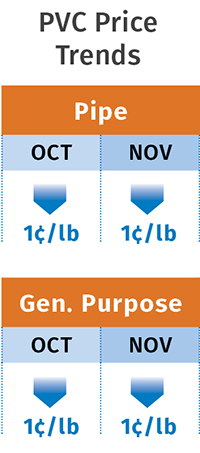

PVC PRICES DOWN

PVC prices dropped another 1¢/lb in October, following a 1¢ drop the previous month. This was in step with the decline in August/September ethylene monomer contract prices. Late-settling October ethylene contracts were likely to be flat, according to RTi’s Kallman.

However, PVC prices were likely to drop another 1¢/lb in November, according to Kallman. He said suppliers are challenged by imports as prices elsewhere dropped. Despite a series of planned PVC plant turnarounds in the September to November, supply was very ample. Kallman ventured that December PVC prices would trend flat to lower.

Related Content

Plastics Processing Activity Drops in November

The drop in plastics activity appears to be driven by a return to accelerated contraction for three closely connected components — new orders, production and backlog.

Read More

Plastics Processing’s Ups and Downs

Overall index dips, but custom processors hold steady. Employment up, backlogs down.

Read More

NPE2024 and the Economy: What PLASTICS' Pineda Has to Say

PLASTICS Chief Economist Perc Pineda shares his thoughts on the economic conditions that will shape the industry as we head into NPE2024.

Read More

Read Next

Troubleshooting Screw and Barrel Wear in Extrusion

Extruder screws and barrels will wear over time. If you are seeing a reduction in specific rate and higher discharge temperatures, wear is the likely culprit.

Read More

Lead the Conversation, Change the Conversation

Coverage of single-use plastics can be both misleading and demoralizing. Here are 10 tips for changing the perception of the plastics industry at your company and in your community.

Read More