The Truth About Reshoring

Reshoring is not just a buzzword, it’s an economically driven correction to a supply chain that had become unbalanced.

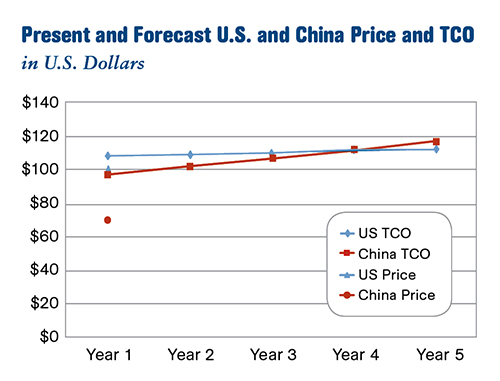

Price isn’t everything: Total Cost of Ownership (TCO) estimator software from the nonprofit Reshoring Initiative shows that when you consider the full costs of manufacturing in China for U.S. consumption, reshoring becomes increasingly competitive.

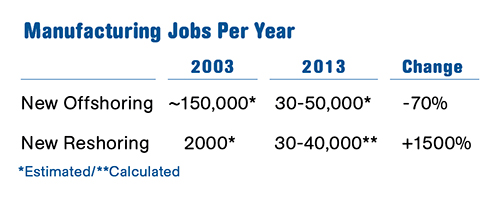

Estimates of the significant turnaround between offshoring and reshoring from 2003-2013 in terms of manufacturing jobs lost or gained. Source: Reshoring Initiative

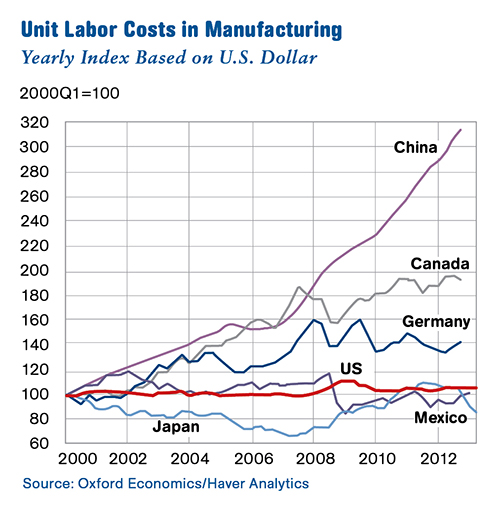

Represented in U.S. dollars, this index shows the unit labor costs for manufacturing since 2000 of six industrialized nations. Unit labor cost in the U.S. dipped following the recession. China’s has been climbing steadily.

The retired chairman of machine-tool company AgieCharmilles LLC, Harry Moser has been a tireless advocate of reshoring since he founded the non-profit Reshoring Initiative.

Talk to a plastics processor these days, and you’re likely to hear a reshoring story; but are these just isolated anecdotes, or do they point to something bigger? In the prevailing sentiment of just a few years ago, much of the plastics industry saw China and low-cost offshore manufacturing as inevitable. But what at one time seemed like an inexorable march eastwards has not only slowed, but in some cases reversed course.

“Reshoring is not a fad,” Frank Russo says. “It’s a real supply-chain strategy based on real economic forces.” Russo is CEO and co-founder of Fabricating.com, a cloud-based sourcing marketplace that offers exclusively American-made custom parts. Russo’s strategy is predicated on a growing market desire for U.S. manufacturing, but others without any “skin in the game” acknowledge that production once lost to places like China has come back, and more new fabrication is staying stateside as well.

“Reshoring is real—and about to dramatically reshape the U.S. economy,” is how Chicago-based audit, tax, and advisory firm Grant Thornton began the executive summary of its November 2013 survey, Realities of Reshoring. That survey of U.S. executives reported that more than one-third of U.S. businesses would move goods and services production back to the U.S. in 2014, with roughly the same percentage planning on “near-shoring” work to places like Mexico. “This means that as much as 5% of overall U.S. procurement may come home,” the survey states.

Ocean freight costs have increased 135%, the Chinese Yuan has gained 18% in value against the dollar, and Chinese manufacturing wages have risen 44%, according to a study by Miami-based Archstone Consulting, part of The Hackett Group. “The perceived 25-40% cost savings associated with offshoring have previously been made possible by low labor costs, cheap commodities, and favorable exchange rates—factors that no longer exist in today’s marketplace,” the study states.

Conversations with processors, consultants, policy advocates, and supply-chain management firms reinforce that viewpoint. Reshoring is not just a buzzword, it’s an economically driven correction to a supply chain that had become unbalanced.

ABSORBING CHINA'S LABOR INFLUX

Offshoring represented “really a 20-year trend of incorporating China into the global economy,” explains Hackett’s David Sievers, strategy and operations practice leader. “So you brought a lot of low-cost labor into the global market; the Chinese government subsidized capacity; and that trend took 20 years to absorb. What we’re seeing now is the logical conclusion of that.”

Going forward, Sievers sees more stability. “The current trend is to having a more balanced production environment on a global basis. Essentially, companies want production close to demand.”

In the last two years, announcements by some of the largest companies in the world regarding their manufacturing footprint support Sievers’ view. Look no further than Apple ($100 million to assemble computers in Texas, with an additional investment in Arizona); big-box retailer Walmart (boosting purchases of U.S.-made goods by $5 billion/yr for 10 years); General Electric (hot-water heater and refrigerator production brought to Kentucky); and Ford Motor Co. (adding capacity for 200,000 vehicles with plans to invest $6.2 billion in U.S. plants by 2015).

In a survey by Accenture, a New York management consulting, technology services, and outsourcing firm, 43% of the manufacturing respondents said they expected to move operations in 2012 and 2013; and in the last two years, 65% of the manufacturers said they had moved some operations. Where? Leading locations were the U.S. (40%), China (28%), and Mexico (21%).

A majority of U.S.-based manufacturing executives at companies with sales in excess of $1 billion told Boston Consulting Group that they are planning to bring back production from China or are actively considering it, according to a September 2013 survey. Fifty-four percent said they would reshore production, up from 37% in a February 2012 poll.

All of these companies rely on suppliers, and their moves have impacted the plastics manufacturing chain. “I see reshoring in our marketplace sometimes several times a week,” Fabricating.com’s Russo says. “Every week, we speak with a buyer that wants to source only in the U.S. They want to reshore work, usually back from China, due to quality-control issues, time to market, delivery issues, language barriers, or to be closer to their customers.”

A MOLDER'S VIEW

Brian Holmes and the custom injection molder he works for take the long view. Holmes is the v.p. of operations and a 34-year veteran at Columbia Plastics Ltd., Surrey, B.C. As offshoring picked up, Columbia pivoted away from the electronics work that was shifting en masse to China, temporarily stemming the tide by adding some assembly work.

“Offshoring really started impacting us in the late ’80s into the ’90s. Then, as things slowed down in 2001, when all of the crises hit at once, that’s really what drove people overseas even faster, companies trying to pare costs out of their systems. From there, that’s when it started getting really tough. If you didn’t have some kind of specialty niche through the early 2000s, that’s when it got tough.”

One niche for Columbia became medical work. The company claims to have the first clean room (ISO Class 7) in Western Canada. That got the company through the lean years and is paying off now as reshoring takes hold. “I’d say there are more inquiries about moving molding back now,” Holmes says. “More people are looking at new stuff and saying, ‘We’re not going to do it over there.’ For people to relocate tools is expensive, no matter where. As products go obsolete they change locations.”

RESHORING'S CHAMPION

Harry Moser’s first experience with offshoring goes back farther than the 1980s and involved a different Asian country. It came in the 1950s and instead of China, the threat was Japan. In high school and college, Moser worked summers at the Singer Sewing Machine Co. in Elizabeth, N.J., starting a lifelong career in manufacturing at the same plant where his father and grandfather had worked. It was there more than 60 years ago that he was shown components sourced from Japan. Moser remembers himself and others laughing a bit at the parts, thinking them crude.

Little did he know then the impact that Japanese competition would have on his employer. “Ten years ago, I drove past the Singer factory,” Moser recalls, “my father and grandfather worked there, I worked there—now nothing is made there.” Opened in 1863 and eventually covering 1.4 million ft², that plant, an icon of American manufacturing, ceased production in 1982 after 109 years.

Moser retired from AgieCharmilles LLC, Lincolnshire, Ill. in 2010 as chairman emeritus after starting at the firm (then called Charmilles Technology) in 1985. Selling equipment around the country over those 25 years, he watched as manufacturers of all shapes, sizes and industries ceased operations.

Back in 2007, Moser started thinking about ways to stem the tide. It was those initial inklings that would lead to his founding of the nonprofit Reshoring Initiative, which he began working on full time in 2010 and incorporated in September 2011. At the very beginning, Moser was asked to give presentations on topics like how to avoid or compete with Southeast Asia.

“What product categories you should go into to avoid Asian competition?” were typical questions Moser addressed. “Talking about things like quick response, rapid design change, and also how to beat them if you have to compete with them.”

As the concept of a Reshoring Initiative coalesced, Moser initially approached the Association For Manufacturing Technology. He won their support, and subsequently that of the National Tool and Machining Association, the Precision Metalforming Association, and the Society of the Plastics Industry (SPI). Gardner Business Media, Inc., Cincinnati, publisher of Plastics Technology, is also a sponsor.

A BETTER COST MODEL

One of the key functions of the initiative today is to move past crude total-cost models that fail to calculate many of the true costs associated with sourcing product from halfway around the world. The initiative created what it calls TCO (Total Cost of Ownership) estimator software, which it offers free to manufacturers to help them construct a real-world model of what companies actually pay for parts.

The TCO concept is catching on, according to Moser, but awareness doesn’t always equate to implementation. Going back to 2009, he says an Archstone survey found that 60% of companies used prices, wage rates, landed costs, or other rudimentary measures. By 2012, he says another survey reported that 60% to 70% of companies put a high priority on using TCO—a number that was encouraging but might be deceiving.

“When I talk to companies about TCO, a typical response might be, ‘We know about it. We have software or a methodology for doing it, but we don’t do it. When it comes time to get the model or plastic parts, we go on costs, because we—the supply-chain people—are rewarded on price not total cost.’”

In that admission, Moser sees an opening. “We still have lots of opportunities,” Moser says. “The good news is most companies don’t do TCO analysis, and all we have to do is educate them. If they were all already using TCO today, then we’d have to change the reality of the economics. Educating buyers is easier than remaking the whole U.S. economy.”

REALITY CHECK

Another function of the Reshoring Initiative is to document reshoring cases reported in the press. Four or five years ago, that amounted to two to three articles per month, according to Moser. Today, the group sees an average of 11 every week, with 115 documented cases of reshoring in 2013. “And we know we missed a lot,” Moser admits. “We get General Motors but we don’t get the injection molder or harness maker—those sorts of things. The question used to be, is it real or a trickle? Is it a trickle or a trend? It’s still not a flood but it is very real.”

Related Content

How to Set Barrel Zone Temps in Injection Molding

Start by picking a target melt temperature, and double-check data sheets for the resin supplier’s recommendations. Now for the rest...

Read More

A Simpler Way to Calculate Shot Size vs. Barrel Capacity

Let’s take another look at this seemingly dull but oh-so-crucial topic.

Read More

Understanding the ‘Science’ of Color

And as with all sciences, there are fundamentals that must be considered to do color right. Here’s a helpful start.

Read MoreRead Next

People 4.0 – How to Get Buy-In from Your Staff for Industry 4.0 Systems

Implementing a production monitoring system as the foundation of a ‘smart factory’ is about integrating people with new technology as much as it is about integrating machines and computers. Here are tips from a company that has gone through the process.

Read More

Processor Turns to AI to Help Keep Machines Humming

At captive processor McConkey, a new generation of artificial intelligence models, highlighted by ChatGPT, is helping it wade through the shortage of skilled labor and keep its production lines churning out good parts.

Read More