Growth Rate Picks Up

Processor business activity increases for eighth of nine months.

.JPG;width=70;height=70;mode=crop;format=webp)

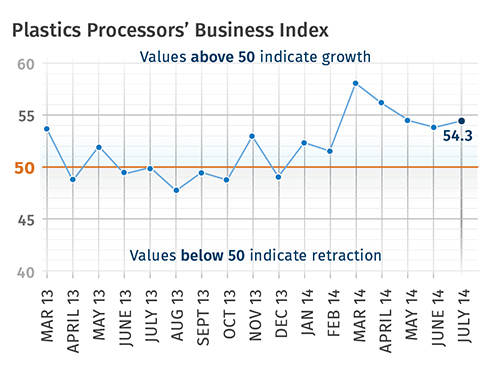

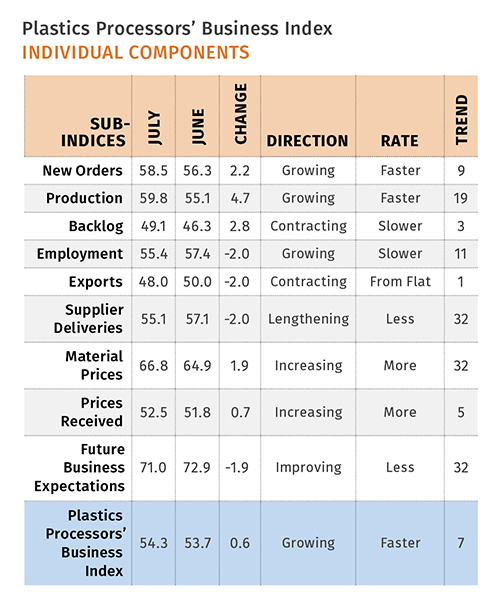

With a reading of 54.3, Gardner’s Plastics Processors’ Business Index showed that the market grew in July for the eighth time in nine months. The rate of growth was slightly stronger in July than June. The index has remained at a relatively high level since March. Compared with July 2013, this July index was 8.6% higher. This is the ninth consecutive month of growth in the month-over-month rate of change. It has grown faster in each of the last two months. The annual rate of change has grown at an accelerating rate each of the last six months.

New orders have grown for nine straight months and are on an uptrend that began last October. Production expanded at a faster rate than in June. Production has expanded every month since December 2012. Backlogs contracted for the third month in a row, but the rate of contraction slowed. Backlogs are still significantly higher than they were a year ago, which is a positive sign for future capacity utilization and capital spending investment. Exports contracted for the first time since April. Supplier deliveries have lengthened at a fairly consistent rate in 2014.

Materials prices have increased at an accelerating rate in the last two months, as have prices received. However, the jump in material prices has been much sharper. Future business expectations remain above their long-run average, though expectations have been sliding consistently since March.

Facilities with more than 50 employees saw better business conditions in July. The most improvement came at facilities with more than 250 employees. But plants with 50-249 employees grew at the fastest rate, with an index above 60.0. Plants with 20-49 employees have grown every month since November 2013. However, they grew at their second slowest rate during that time in July. Plants with fewer than 19 employees contracted for the third time in four months, but July had the slowest rate of contraction of those months. Every region expanded in July. The North Central–East was by far the fastest growing region.

Capital spending plans fell below $1 million for the first time since February. However, they were still about 13% above the historical average in July. Compared with a year ago, capital spending plans were down 15.4%. This is the fastest rate of month-over-month contraction since the index began in December 2011. The annual rate of change is still growing at a significant rate, but the rate of growth has fallen sharply since November 2013.

Related Content

-

Plastics Processing Contracts Again

October’s reading marks four straight months of contraction.

-

Processing Slips as Summer Simmers

Monthly index suggests slower growth in June for plastics processors overall and contraction for custom firms.

-

Processing Activity Contracts More Slowly in January

Despite contracting again in January, plastics processing activity rebounded a bit from a rather significant drop in December.