Processing Expansion Returns to Near All-Time High

Industry smashes records in first half of 2021.

.jpg;width=70;height=70;mode=crop;format=webp)

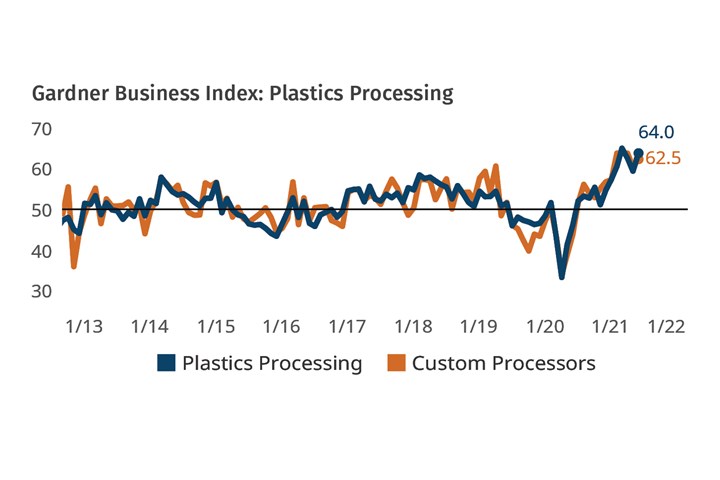

The Gardner Business Index (GBI) for plastics processing finished June at 64, returning to near-record levels after slipping in April and May. The latest reading was driven by higher levels of backlogs, new orders, production, employment, and export orders. During just the first half of 2021, the Index reported four months in which all components expanded. Strengthening activity readings between late 2020 and now have sent both business sentiment and expected capital-spending plans to multi-year highs in recent months. The Index is based on monthly surveys of subscribers to Plastics Technology magazine.

FIG 1 June’s gains were broad-based, with all six index components moving higher. The biggest gains were in employment, new orders, and production.

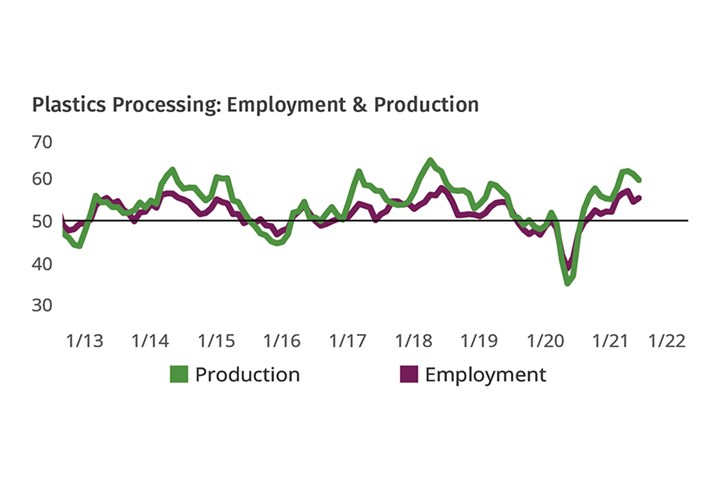

Custom processors thus far in 2021 have reported consistently slowing growth in new orders during the second quarter and generally unchanged foreign orders. During the first half of 2021, processors overall (including captive shops) and custom processors in particular reported surging backlog activity, in part due to difficult production conditions and hiring challenges. These challenges have generated an enduring spread between new orders and production activity, which has sent each monthly backlog reading during the second quarter to all-time high levels.

FIG 2 While employment and production both accelerated in the first half of 2021, a more rapid rise in new orders resulted in a string of monthly all-time-high backlog readings during the second quarter.

EDITOR’S NOTE: Finding reliable and relevant data to help guide your business is always important, but especially so during challenging economic times. For this reason, the GBI Plastics Processing and Custom Processing Indices serve as a great tool for making data-driven decisions. Thank you to everyone who has previously completed GBI surveys. Your participation helped increased response counts by 15% in 2020, making the GBI better than ever because of your involvement. Thank you for your time and efforts and for trusting us to provide you with the latest industry and business insights both in the past and in the future.

If you are a North American plastics processor and would like to participate in this research, click here to begin the process by subscribing free to Plastics Technology magazine.

ABOUT THE AUTHOR: Michael Guckes is chief economist and director of analytics for Gardner Intelligence, a division of Gardner Business Media, Cincinnati. He has performed economic analysis, modeling, and forecasting work for more than 20 years among a wide range of industries. He received his BA in political science and economics from Kenyon College and his MBA from Ohio State University. Contact: (513) 527-8800; mguckes@gardnerweb.com.

Related Content

-

Plastics Processing Continued Contraction in April

Despite some index components accelerating and others leveling off, April spelled contraction for overall plastics processing activity.

-

Plastics Processing Contracts Again

October’s reading marks four straight months of contraction.

-

Plastics Processing Business Index Contracts Further

All components dip as index hits low point of 2023.

.png;maxWidth=300;quality=90;format=webp)