PE Film Market Analysis: Institutional Can Liners

Huge market still overwhelmingly dominated by monolayer structures.

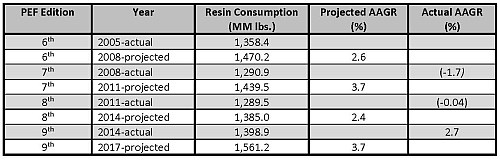

During 2014, approximately 1.398 billion lb. of PE was consumed in the production of institutional trash bags. With an average annual growth rate (AAGR) of 3.7%, this market is expected to increase to 1.561 billion lbs of PE resin consumption by 2017.

These are among the conclusions of the most recent study of the PE Film market conducted by Mastio & Co., St. Joseph, Mo.

Widths of institutional trash bags range from 13 to 69 in., with the most typical width being 30 in. Institutional trash bag lengths vary from 17 in. to 90 in., with the average length being 48 in. Institutional trash bag capacities range from 4 gal to 90 gal, with 33, 40, and 45 gal being the most common, Mastio notes.

Institutional trash bag film gauges range from 0.1 mil to 10 mils in the United States (U.S.) and 0.3 mil to 12.8 mils in Canada. Many producers stated there is not a typical gauge for institutional trash bags as the film gauge depends on the application, Mastio points out.

MATERIALS TRENDS

Many institutional can liner processors are beginning to use biodegradable resins such as polylactic acid (PLA) and synthetic polyesters in the production of institutional trash bags. PLA is a corn-derived biodegradable plastic that is designed to biodegrade in any standard compost bin. That said, none of the processors who participated in the Mastio study reported any use of PLA resin in the production of can liners during 2014.

Mastio reports that the resin most commonly utilized for institutional trash bags in 2014 was LLDPE. LLDPE provides added strength and tear resistance over low density PE (LDPE) resin, which makes the film less apt to puncture. LLDPE can be further down gauged without sacrificing strength. Various grades of LLDPE resins utilized in this market include the following: LLDPE-hexene, LLDPE-butene, LLDPE-octene, mLLDPE, and LLDPE-super hexene.

High density PE (HDPE) was the second most utilized material in this market during 2014. High molecular weight-HDPE (HMW-HDPE) and medium molecular weight-HDPE (MMW-HDPE) resins allow processors to manufacture institutional trash bags in thinner gauges that are about three times stronger and more durable than other trash bags constructed with LLDPE, LDPE, and/or medium density PE (MDPE), according to Mastio HDPE provides the highest level of puncture resistance of all PE resin material. However, HDPE requires more costly, specialized film extrusion equipment and is more difficult to extrude. Several film processors in this market lack the specialized film extrusion equipment needed to process HDPE materials.

Post-consumer reclaim was the third most commonly utilized material in the production of institutional trash bags during 2014. The reported utilization of PCR included post-industrial scrap resins consisting of PCR-LLDPE, PCR-LDPE and mixed PCR-PE (HDPE, LDPE, LLDPE and MDPE). Cost savings and adherence to mandates of PCR content by a few states, such as California; have also contributed to increased use of PCR in this market.

LDPE is also utilized in this market, mostly in blends with LLDPE and in multi-layer coextrusions. One advantage of utilizing LDPE resin is increased bag clarity, which is important for bags used in recycling programs. Also, LDPE resin, when used alone or in blends, has increased processing ease.

Utilization of LDPE-homopolymer, LDPE-ethylene-vinyl acetate copolymer (LDPE-EVA copolymer), and LDPE-ethylene-methyl acrylate copolymer (LDPE-EMA copolymer) grades were reported in this market during 2014.

TECHNOLOGY TRENDS

Monolayer blown film constructions remain the principal design for institutional trash bags, accounting for more than 94.3% of PE resin consumption.

MY TWO CENTS

It’s a bit surprising that monolayer structures are still the technology of choice in this market. It suggests to me that equipment assets in this market are aging. As more film-recycling streams start to develop, it’s possible that institutional liner companies will add more coextrusion capacity. As the report suggests, many are using PCR now, but apparently in blends with prime resin in single-layer structures.

Related Content

Avoid Four Common Traps In Granulation

Today, more than ever, granulation is an important step in the total production process. Our expert explains a few of the many common traps to avoid when thinking about granulators

Read More

Understanding the ‘Science’ of Color

And as with all sciences, there are fundamentals that must be considered to do color right. Here’s a helpful start.

Read More

How to Estimate and Control Head Pressure

You rightfully worry about melt temperature, but don’t overlook head pressure, because the two are closely linked and will influence line performance.

Read More

Cooling the Feed Throat and Screw: How Much Water Do You Need?

It’s one of the biggest quandaries in extrusion, as there is little or nothing published to give operators some guidance. So let’s try to shed some light on this trial-and-error process.

Read MoreRead Next

People 4.0 – How to Get Buy-In from Your Staff for Industry 4.0 Systems

Implementing a production monitoring system as the foundation of a ‘smart factory’ is about integrating people with new technology as much as it is about integrating machines and computers. Here are tips from a company that has gone through the process.

Read More

Processor Turns to AI to Help Keep Machines Humming

At captive processor McConkey, a new generation of artificial intelligence models, highlighted by ChatGPT, is helping it wade through the shortage of skilled labor and keep its production lines churning out good parts.

Read More

Troubleshooting Screw and Barrel Wear in Extrusion

Extruder screws and barrels will wear over time. If you are seeing a reduction in specific rate and higher discharge temperatures, wear is the likely culprit.

Read More